The Complete DeFi Tax Guide: Staking, Swaps, LPs, Airdrops, and More

Every DeFi interaction is a potential taxable event. Learn how staking rewards, DEX swaps, liquidity pools, airdrops, bridges, and gas fees are taxed under IRS rules.

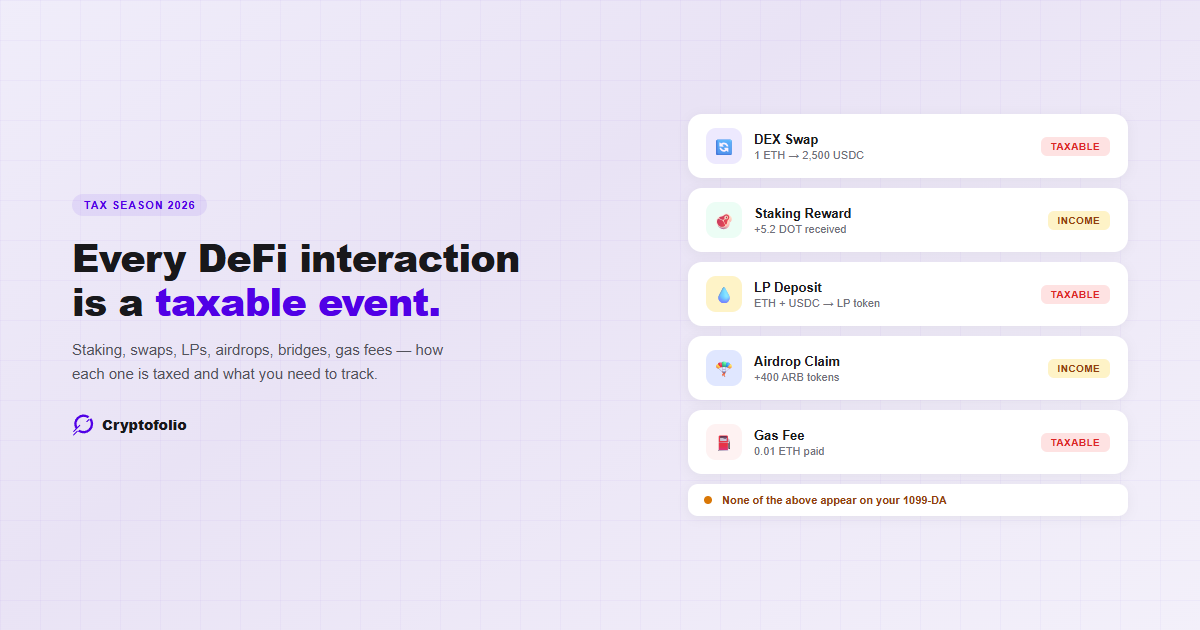

If you staked tokens, swapped on a DEX, provided liquidity, claimed an airdrop, bridged to another chain, or even just paid gas fees in 2025, every single one of those interactions is a potential taxable event under US tax law.

And here's the problem: most of them won't show up on your 1099-DA.

Under IRS Notice 2024-57, many DeFi transactions are temporarily excluded from broker reporting requirements. That doesn't mean they're tax-free. It means you're responsible for tracking and reporting them yourself.

This guide breaks down every major DeFi transaction type, explains how it's taxed, and shows what you need to track for each one.

The Core Principle: Crypto Is Property

The IRS treats all digital assets as property, not currency or securities. Every time you dispose of a digital asset by selling, swapping, spending, or using it to pay fees, you trigger a taxable event.

The gain or loss is the difference between what you received (the amount realized) and what you originally paid (your cost basis), calculated using FIFO or another permitted method from your wallet's lot queue. (For a full comparison of FIFO, LIFO, and Specific Identification, see our accounting methods guide.)

A "disposal" in the DeFi context is much broader than just selling for USD. Swapping ETH for USDC on Uniswap? Disposal. Using ETH to pay gas? Disposal. Adding tokens to a liquidity pool? Likely a disposal. Each one requires a cost basis calculation.

(If you need a refresher on how cost basis and FIFO work, see our cost basis guide.) Realized losses from DeFi positions offset capital gains across your entire portfolio, including stocks. See the full loss netting rule.

Token Swaps on DEXs

Tax treatment: A swap is a taxable disposition of the token you give up, and an acquisition of the token you receive.

When you swap ETH for USDC on Uniswap, two things happen simultaneously for tax purposes:

- You dispose of ETH. Your gain or loss is calculated using the fair market value of what you received (the USDC) minus the FIFO cost basis of the ETH you gave up.

- You acquire USDC. Your cost basis for the USDC is its fair market value at the time of the swap.

Critical point: Swapping into a stablecoin does not defer your gain. Under IRS property rules, the gain is recognized at the moment of the swap, not when you later convert USDC to USD. This is one of the most misunderstood aspects of crypto taxation. For a deeper look at how stablecoin swaps, depegs, and yield are treated, see our full stablecoin tax guide.

What about transaction costs on swaps? If you pay gas fees or DEX fees in a digital asset (like ETH) to execute the swap, those fees reduce the amount realized on the asset you're disposing of. The gas fee payment itself is also a separate disposal of the fee asset (usually ETH) through your FIFO queue. So a single swap can actually trigger two separate gain/loss calculations: one for the primary swap and one for the gas fee.

Staking Rewards

Tax treatment: Receiving staking rewards is ordinary income at fair market value when you gain dominion and control. That FMV becomes your cost basis for any future sale.

When your staked SOL, DOT, ETH, or any other token generates rewards, the IRS treats each reward as income the moment you can access it. You don't need to sell it for the income to be taxable.

Liquid staking: Protocols like Lido (stETH) and Rocket Pool (rETH) add complexity. When you deposit ETH and receive stETH, this may be treated as a swap (disposing of ETH, acquiring stETH at FMV). As stETH rebases and your balance increases, the additional tokens may be treated as income.

The IRS has not issued specific guidance on liquid staking mechanics. Some legal interpretations argue that minting or redeeming liquid staking tokens may not constitute a taxable event, but this view has not been formally adopted by the IRS. A conservative approach is to treat each rebase increment as income at FMV when received, similar to standard staking rewards. Consult a tax professional for your specific situation.

For a detailed look at how staking rewards create individual tax lots, why per-wallet tracking matters, and what most trackers get wrong when you are staking across multiple protocols, see our guide on tracking staking rewards across wallets.

Liquidity Pools

Tax treatment: Adding liquidity is generally treated as disposing of the tokens you contribute and acquiring LP tokens. Removing liquidity reverses this. Both are taxable events.

This is one of the most complex areas of DeFi taxation. Here's how it works:

Adding Liquidity

When you deposit ETH + USDC into a Uniswap pool and receive LP tokens:

- You dispose of ETH. Calculate gain/loss using FIFO basis vs. the FMV of the LP tokens received (allocated proportionally).

- You dispose of USDC. Calculate gain/loss (usually near zero for stablecoins).

- You acquire LP tokens. Cost basis equals the total FMV of the LP tokens received. Holding period starts the day after receipt.

Removing Liquidity

When you redeem your LP tokens for ETH + USDC:

- You dispose of the LP tokens. Calculate gain/loss using FIFO basis vs. FMV of the tokens received.

- You acquire ETH. Cost basis equals FMV at time of receipt.

- You acquire USDC. Cost basis equals FMV at time of receipt.

Impermanent loss is not a separately recognized tax event. The economic loss is captured in the gain/loss calculation when you remove liquidity, because the composition and value of the tokens you receive back will differ from what you originally deposited.

Yield farming rewards earned on top of LP positions (like CAKE, SUSHI, or protocol governance tokens) follow the same rules as staking rewards: ordinary income at FMV when received, which becomes your cost basis.

Airdrops and Forks

Tax treatment: Receiving airdropped tokens is generally ordinary income at fair market value when you gain dominion and control.

Airdrops

When a protocol sends you governance tokens (like UNI, ENS, or ARB airdrops), the IRS treats this as income if you can access and use the tokens. The taxable moment is when you have the ability to transfer, sell, or otherwise exercise control over them, not necessarily when they appear in your wallet if there's a claim step.

- If you need to claim: income is recognized when you claim and receive the tokens.

- If tokens are deposited directly: income is recognized when you can access them.

Forks

A hard fork by itself is not necessarily a taxable event. If the fork results in you receiving new tokens that you have dominion and control over, those new tokens are generally treated as ordinary income at FMV at the time you gain access. If you receive nothing from the fork (e.g., you didn't hold the asset on the relevant chain), no tax event occurs.

For a detailed guide on how airdrops are taxed and the double-taxation trap most people miss, see our airdrop tax guide.

Bridge Transfers

Tax treatment: Bridging assets between chains you control is generally a transfer, not a taxable disposition. But bridge fees are taxable.

Moving ETH from Ethereum to Arbitrum, or USDC from Ethereum to Polygon, is treated like moving crypto between your own wallets. The cost basis and holding period carry over from the source chain to the destination chain.

However, bridge fees add complexity:

Bridge fees paid in crypto (like ETH gas to initiate the bridge) are a disposal of the fee asset. You need to calculate gain/loss on the ETH used for gas, using FIFO against your ETH lots on the source chain.

This is easy to overlook because the bridge "just moves" your assets. But every gas payment is a micro-disposal that goes through your FIFO queue.

Gas Fees

Tax treatment: Every gas fee paid in a digital asset is a disposal of that asset, triggering a gain/loss calculation.

This is the most frequently missed taxable event in DeFi. Every time you pay gas in ETH (or AVAX, SOL, MATIC, BNB, etc.), you are disposing of that asset in exchange for transaction services. The fair market value of the gas at the time of payment determines the amount realized, and the FIFO cost basis of the gas tokens determines your gain or loss.

How gas fees interact with other transactions:

- Gas to execute a purchase: The gas cost is added to the cost basis of the asset you're acquiring.

- Gas to execute a sale or swap: The gas cost reduces the amount realized on the asset you're disposing of.

- Gas for a self-transfer or bridge: The transfer itself isn't taxable, but the gas fee is still a disposal of the fee asset. In this case, the gas fee is not a "digital asset transaction cost" that adjusts basis or proceeds. It is a standalone disposal for services.

- Gas for a failed transaction: Still taxable. You paid for transaction services; the fact that the transaction failed doesn't change the tax treatment of the gas asset disposal.

For active DeFi users making dozens of transactions per week, gas fee disposals can add up to significant cumulative gains or losses. For a detailed breakdown of how gas fees hit your FIFO queue, the different rules by transaction type, and why most trackers miss this entirely, see our guide on how gas fees affect your cost basis.

Wrapping and Unwrapping Tokens

Tax treatment: Wrapping ETH to WETH (or similar wrapping events) is a gray area. Conservative treatment is to treat it as a taxable swap.

When you wrap ETH to WETH, you're exchanging one token for another. Under strict property rules, this could be treated as a disposition of ETH and acquisition of WETH at FMV. In practice, the gain or loss is typically near zero if the wrap is done immediately, but it still creates a new tax lot with a potentially different basis if ETH's price has changed since you acquired it.

The IRS has not issued specific guidance on wrapping. Under Notice 2024-57, wrapping and unwrapping transactions are among those temporarily excluded from 1099-DA reporting, which suggests the IRS recognizes these as a distinct category that may receive specific guidance in the future.

Conservative approach: Treat wrapping as a swap (disposal + acquisition). Track the new WETH lot with basis equal to FMV at time of wrapping. This creates a clean audit trail.

For a detailed look at both tax positions on wrapping, how your cost basis carries through under each approach, and where most trackers break, see our guide on what happens to your cost basis when you wrap crypto. For how the SEC's 2026 interpretation addresses the securities status of staking, wrapping, and airdrops, see our SEC taxonomy overview.

What Won't Show Up on Your 1099-DA

Under IRS Notice 2024-57, the following DeFi transactions are temporarily excluded from broker reporting on Form 1099-DA until the Treasury Department and IRS issue further guidance:

- Wrapping and unwrapping transactions (e.g., ETH to WETH)

- Liquidity provider transactions (adding/removing liquidity, minting/burning LP tokens)

- Staking transactions (including liquid staking and restaking)

- Lending of digital assets

- Short sales of digital assets

- Notional principal contract transactions

Note: This reporting exception does not apply to compensation earned by participants in these transactions. For example, staking rewards may still be reported on Form 1099-MISC.

This means your 1099-DA from Coinbase, Kraken, or other custodial exchanges will not reflect most of your DeFi activity. But every transaction listed above is still a taxable event that you must report on your tax return.

This is the gap that makes DeFi tax compliance so difficult. Your broker reports your centralized exchange activity. Everything else, including DEX swaps, staking rewards, LP positions, airdrops, bridges, and gas fees, is entirely on you to track and report.

(For more on what does and doesn't appear on your 1099-DA, see our 1099-DA explainer.)

How to Track All of This

The volume of taxable events in DeFi makes manual tracking impractical. A single yield farming session can generate dozens of taxable events: the initial swap, the LP deposit, daily reward claims, gas fees on every interaction, and the eventual LP withdrawal and swap back. For a detailed walkthrough of how cost basis changes at each step of a DeFi interaction, see our DeFi cost basis guide. For a guide on how to track DeFi positions across multiple protocols, including what to look for in a tracker and the mistakes most tools make, see our DeFi tracking guide.

Each event needs:

- A timestamp

- The fair market value in USD at that exact moment

- The cost basis of any asset disposed (from the correct wallet's FIFO queue)

- The creation of new tax lots for assets received

- Classification as ordinary income or capital gain/loss

Cryptofolio automates this entire process. It connects to your wallets and on-chain data, parses every DeFi protocol interaction, and maintains accurate FIFO lot queues on a per-wallet basis. Staking rewards, LP entries and exits, bridge transfers, DEX swaps, airdrops, and gas fees are all tracked and classified automatically.

When a protocol interaction can't be fully parsed (for example, a new or unsupported protocol), Cryptofolio flags it in the UI rather than silently guessing, so you always know exactly where your tax data stands.

DeFi taxes are complex. Tracking them shouldn't be.

Cryptofolio automatically parses every DeFi protocol interaction and maintains accurate FIFO lot queues across all your wallets.

The Bottom Line

DeFi gives you unprecedented control over your finances. It also gives you unprecedented tax complexity. Every swap, stake, deposit, withdrawal, claim, bridge, and gas payment is a taxable event that needs to be tracked with precision.

The IRS isn't ignoring DeFi activity. They've simply deferred the reporting requirements while they figure out the rules. Your obligation to report accurately exists regardless of whether your broker sends you a form.

The cost of getting this wrong ranges from overpaying taxes (because you couldn't prove your cost basis) to IRS notices and penalties (because your reported numbers don't add up). The cost of getting it right is proper tracking from the start.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. While we strive to keep our content accurate and up to date, information in this article may become outdated as policies evolve. Consult a qualified tax professional for advice on your individual circumstances.