Stablecoins Were Coined Digital Dollars. The IRS Calls Them Property.

Stablecoins are property under IRS rules. Every USDC swap is a disposal. Learn how depegs, worthlessness rules after OBBBA, and the PARITY Act affect your taxes.

Stablecoins feel like cash. USDC, USDT, and DAI are pegged to the dollar, marketed as safe harbor, and used across crypto as dollar equivalents. Every major exchange lets you hold them, spend them, and swap them like currency.

The IRS treats every one of those actions as a taxable event.

Under US tax rules, stablecoins are property. Every swap is a disposal. Every depeg creates real gains and losses that belong on Form 8949, regardless of whether the final dollar value moved. Most portfolio trackers do not record any of it.

Stablecoins Are Property, Not Dollars

The IRS classified virtual currencies as property in Notice 2014-21, and stablecoins fit that definition. The 2024 final regulations on digital asset broker reporting include stablecoins within the definition of “digital asset” and the classification has not changed.

The practical consequence is simple. Every stablecoin transaction is a taxable disposal. Swap USDC for USDT, you disposed of the USDC. Use USDC to buy ETH, you disposed of the USDC. Use USDC to pay for something, you disposed of the USDC. Each one goes on Form 8949 with its own cost basis and proceeds.

Here is what that looks like in numbers. You buy 10,000 USDC for exactly $10,000 on Monday. On Tuesday, USDC is trading at $0.9997 and you swap it for 9,997 USDT. You just realized a $3 capital loss. On its own, that's a rounding error. Run it across a year of active DeFi activity with hundreds of stablecoin legs through swaps, LP positions, and yield claims, and the reportable transaction count is in the thousands. Each one belongs on Form 8949.

Yield works the other way. USDC earned from Aave, USDT rewards from a protocol, stablecoins received as payment for work. These are ordinary income at fair market value on the day received, and that value becomes the cost basis for the new lot. Our guide to cost basis explains the mechanics for any digital asset.

What Happens During a Depeg

Stablecoins depeg more often than most holders realize. Most events are minor. Two of them produced real, documented tax consequences for millions of holders.

Terra UST, May 2022. TerraUSD was one of the largest stablecoins in the market, with roughly $17.5 billion in circulating supply. Starting May 7, 2022, large UST sales in Curve's 3pool broke the peg. Within days, UST plunged to around $0.10 and LUNA's supply hyperinflated into the trillions. The combined market cap loss was roughly $45 billion. Holders who sold into the collapse locked in capital losses. Holders who waited for a recovery are still waiting.

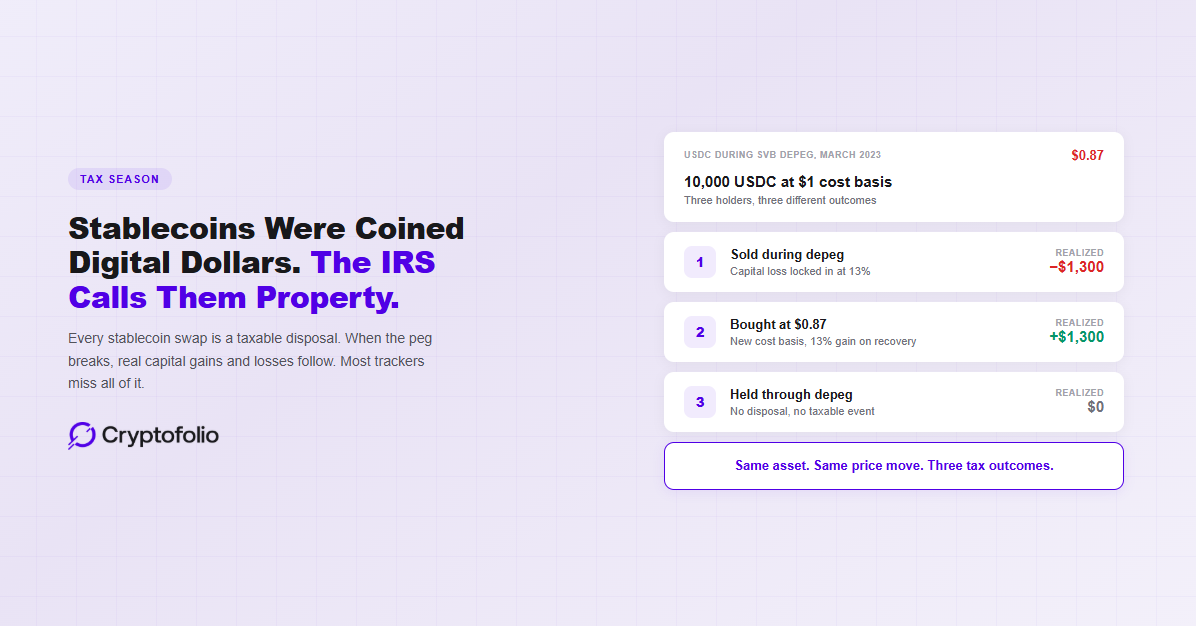

USDC during the SVB crisis, March 2023. Circle held $3.3 billion of its roughly $40 billion in reserves at Silicon Valley Bank. When SVB was taken into FDIC receivership on Friday, March 10, USDC fell to around $0.87 by Saturday morning. Federal intervention restored confidence over the weekend, and the peg was back by Monday. Panic sellers locked in roughly 13% capital losses. Buyers at $0.87 who held through the recovery booked 13% gains.

These are not edge cases. They affected millions of holders on both the loss side and the gain side.

The Three Tax Scenarios During a Depeg

Every depeg creates three possible outcomes depending on what you did with the position.

Sell during the depeg. If you held USDC at a $1 cost basis and sold at $0.87, you realized a 13% capital loss. Capital losses offset capital gains first, then up to $3,000 of ordinary income per year. Anything left over carries forward indefinitely.

Buy during the depeg. If you bought USDC at $0.87 and held through the recovery to $1, your new cost basis is $0.87. When you sell, the gain is calculated from that lower number. Sell within a year and it's short-term at ordinary income rates. Hold longer than a year and it's long-term at preferential rates.

Hold through the depeg with no transaction. No taxable event. The unrealized loss exists on paper, but until you dispose of the asset, there is nothing to report. This is true even if the depeg drops the price by 99%.

Worthless Is Not a Deduction

When a stablecoin collapses completely, most holders assume the worthless tokens in their wallet become an automatic write-off. They don't.

The IRS ruled on this in January 2023. The position: a coin that is almost worthless is not the same as worthless. As long as the token still trades somewhere and you still control the position, you have not taken a deductible loss. You have an asset that dropped in value.

The rule got harder, not easier, in 2025. The Tax Cuts and Jobs Act had suspended the category of deduction these losses fall into, with the suspension set to expire at the end of 2025. A lot of crypto content assumed worthlessness deductions would come back in 2026. They did not. The One Big Beautiful Bill Act made the disallowance permanent.

The practical path is different. A capital loss is not in the same category. If you sell or exchange a collapsed stablecoin for anything at all, even a fractional cent, you realize a capital loss on Form 8949 and Schedule D. That loss is deductible against gains and up to $3,000 of ordinary income per year with unlimited carryforward. Holding a worthless coin gets you nothing. Selling it for a penny gets you the full loss. Those capital losses offset gains across every capital asset you hold, including stocks. See the full netting rule.

Theft losses are different. Those sit in a separate category and remain potentially deductible when properly documented. Our post on DeFi protocol hacks covers the theft loss framework.

What Most Trackers Get Wrong

A DeFi user generates hundreds of stablecoin transactions a year. Sometimes thousands. Most portfolio trackers miss most of them.

Stablecoin-to-stablecoin swaps treated as transfers. A USDC-to-USDT swap at $0.9998 is a disposal at a $0.0002 per-unit loss. On a $10,000 swap, that's $2 of reportable loss. Thousands of times a year, those compound into real numbers. Trackers that treat these as internal transfers miss every one.

DEX swaps routed through stablecoin legs. When you swap ETH for SOL on an aggregator, the route often passes through USDC or USDT. The conservative tax position treats that as two disposals, not one. Trackers that record only the input-to-output pair corrupt the FIFO queue for your stablecoin position.

Yield received without a new cost basis stamp. USDC earned as yield is ordinary income at fair market value on the day received. That value becomes the cost basis of a new lot. Trackers that pool all incoming USDC into a single balance lose per-lot basis, which breaks every future calculation.

Depeg pricing stuck at the reference. During the SVB depeg, USDC was below its peg for roughly 36 hours. Trackers that default to $1 showed wrong portfolio values for the entire window. A holder selling at $0.87 was recording a loss the tracker didn't reflect.

Stablecoins in DeFi Make It Worse

Every DeFi protocol that touches stablecoins adds complexity. Adding liquidity to a USDC/USDT pool is potentially two disposals, depending on which position you take on LP deposit tax treatment. Lending USDC on Aave generates yield denominated in the stablecoin, which creates ordinary income with its own cost basis when received. Bridging USDC between chains may or may not be a taxable event, again depending on the position you take.

Stablecoins are supposed to simplify DeFi by removing price volatility. For tax purposes they do the opposite. Every interaction is potentially a taxable event, and every taxable event needs documentation that most trackers do not generate. Our DeFi cost basis guide covers where these events happen.

Legislation That Could Change This

Two pieces of proposed legislation address stablecoins from different angles. Neither has become law as of April 2026.

The CLARITY Act passed the House in July 2025 and is currently stalled in the Senate. It is primarily a market structure bill that sets jurisdictional lines between the SEC and CFTC and defines what qualifies as a digital commodity. The Senate Banking Committee's draft that builds on CLARITY has added stablecoin yield provisions that would ban passive yield while allowing activity-linked rewards, though those are contested and have delayed Senate action. CLARITY does not change how stablecoins are taxed. Under any version of CLARITY that has been publicly released, every swap is still a disposal.

The PARITY Act is the bill that would actually change tax treatment. It is a bipartisan discussion draft from Representatives Horsford and Miller, re-introduced in late March 2026. Its current text would stop recognizing gains or losses on stablecoin sales when the taxpayer's cost basis is within 1% of the redemption value, which would exempt most everyday stablecoin activity from tax reporting. It would also apply wash sale rules to digital assets for the first time.

Right now, neither is law. The current IRS treatment applies to every stablecoin transaction you have already made this year.

How Cryptofolio Handles This

Cryptofolio tracks every stablecoin transaction as a separate disposal with its own cost basis and proceeds, regardless of how close the value is to the peg. A USDC-to-USDT swap at $0.9998 is recorded as a disposal with a $0.0002 per-unit loss. DEX swaps that route through stablecoin legs are tracked as two disposals, not one.

Yield received in stablecoins is recorded as ordinary income at fair market value on the day received, and that value becomes the cost basis for the new lot.

During depeg events, Cryptofolio pulls the actual market price rather than defaulting to the pegged reference. If USDC is trading at $0.87, that is the price used for valuation and accounting.

Stablecoin transactions add up faster than any other asset class. Cryptofolio tracks every one.

Most trackers treat stablecoins as dollar-equivalents. Cryptofolio treats them the way the IRS does.

The Bottom Line

Stablecoins were built to feel like cash. Under US tax rules, they are not treated like cash. Every swap, every trade, every payment creates a reportable event with real cost basis consequences. Depegs turn those events into meaningful gains or losses, and worthless coins in your wallet do nothing for you unless you sell them.

Two proposals in Congress could change this. Neither has passed. Until one does, Form 8949 expects a line item for every transaction. A tracker that treats USDC as dollar-equivalent is showing you a version of your portfolio that doesn't match what the IRS sees. That mismatch is where audit risk, overpayment, and reporting failures live.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, financial, or investment advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. While we strive to keep our content accurate and up to date, information in this article may become outdated as policies evolve. Consult a qualified professional for advice on your individual circumstances.