1099-DA Crypto Explained: What to Do About Missing Cost Basis

Millions of crypto investors are receiving IRS Form 1099-DA for the first time. Learn what it means, why cost basis is missing, and how to fix it before filing.

What Is Form 1099-DA?

Form 1099-DA is a new IRS tax form specifically designed for digital asset transactions. Starting with the 2025 tax year (filed in 2026), centralized crypto exchanges and brokers are required to issue this form to users who sold, traded, or disposed of digital assets during the year.

Think of it like a 1099-B for stocks, but for crypto. It reports the gross proceeds from each transaction to the IRS. If your exchange has sufficient data, it may also report your cost basis (what you originally paid for the asset). But here's the problem: most of the time, it doesn't.

The form is part of the IRS's broader effort to close the "crypto tax gap." According to Treasury estimates, billions in crypto gains go unreported each year. The 1099-DA is designed to change that by creating a paper trail between exchanges and the IRS.

Starting with tax year 2025 (filed in 2026), centralized brokers are required to report gross proceeds from crypto dispositions on Form 1099-DA. Brokers must furnish 1099-DA statements to recipients by February 17, 2026, though some platforms like Coinbase may deliver by March 17. Cost basis reporting becomes mandatory for assets acquired after January 1, 2026, meaning most filers this year will see cost basis fields left blank.

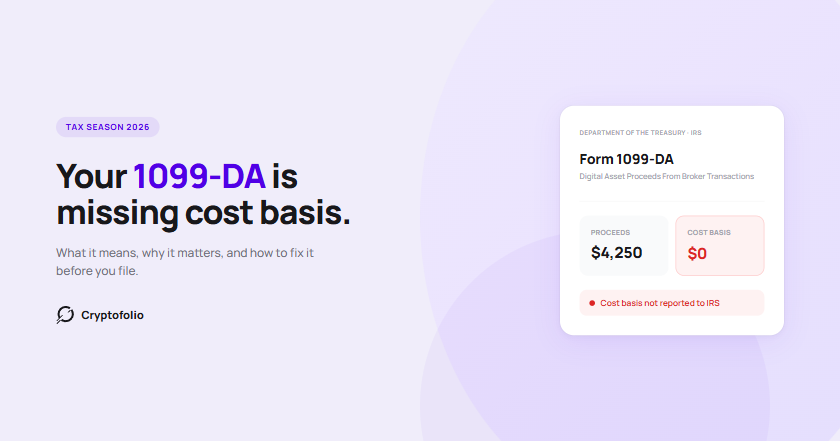

Why Your Cost Basis Is Probably Missing

If you've already received your 1099-DA, you may have noticed something alarming: the cost basis field is either blank or listed as "N/A." Here's what that looks like in practice:

This doesn't mean you owe taxes on the full $4,250. It means your exchange doesn't have enough information to calculate what you originally paid for the asset. Without cost basis, the IRS may assume your basis is $0, meaning you'd owe taxes on the entire proceeds amount as if it were pure profit.

There are several reasons why cost basis is commonly missing:

- You transferred crypto from another exchange or wallet. When you move Bitcoin from Coinbase to Kraken and then sell on Kraken, Kraken has no idea what you originally paid on Coinbase.

- You acquired crypto before exchanges tracked cost basis. Many exchanges only started tracking purchase prices recently. Older holdings have no recorded basis.

- You received crypto from DeFi, airdrops, or mining. These acquisition methods happen outside of centralized exchanges, so there's no purchase record.

- Exchanges aren't required to report cost basis yet. For assets acquired before January 1, 2026, brokers are not required to report cost basis on the 1099-DA, only proceeds.

The Cost Basis Problem Gets Worse With Transfers

The cost basis gap is most severe when you've moved crypto between platforms. Consider this common scenario:

- You buy 1 ETH on Coinbase for $1,800 in 2023.

- You transfer that ETH to a MetaMask wallet.

- You later send it to Kraken and sell it for $4,250 in 2025.

Kraken will report the $4,250 in proceeds on your 1099-DA. But it has no way of knowing you originally paid $1,800 on Coinbase. Without that information, the IRS sees $4,250 in proceeds and $0 in cost basis, resulting in a $4,250 taxable gain instead of the actual $2,450 gain.

This problem multiplies with every transfer. If you've used multiple wallets, DEXs, bridges, or staking protocols, the trail becomes even harder to follow. Token swaps on Uniswap, liquidity pool deposits and withdrawals, bridge transfers between chains, staking rewards, and airdrops all create new cost basis events that centralized exchanges can't see. Each hop strips away the cost basis information that ties back to your original purchase.

For a deep dive on how transfers break your cost basis and how to fix it, see our transfer guide.

It's also worth noting that under IRS Notice 2024-57, certain DeFi transactions are temporarily excluded from 1099-DA reporting. This includes wrapping and unwrapping tokens, liquidity pool lending, and staking. While these transactions won't appear on a 1099-DA, they are still taxable events and need to be tracked for accurate cost basis reporting. For a complete breakdown of how DeFi transactions are taxed, see our DeFi tax guide.

What You Need to Do Before Filing

The good news: you're not stuck with whatever your 1099-DA says. The IRS allows you to report your own cost basis, but you need records to back it up. Here's what to do:

1. Gather your transaction history from every platform

Download CSV exports from every exchange you've used, including Coinbase, Kraken, Binance, Gemini, etc. If you've used DeFi protocols, pull your on-chain transaction history from Etherscan, Solscan, or similar block explorers.

2. Match transfers across platforms

This is the hardest part. You need to link each transfer-out from one platform to the corresponding transfer-in on another. This "transaction binding" is what connects your original purchase price to the final sale, even if the asset moved through three wallets along the way.

3. Calculate your actual cost basis

For each asset you sold, determine what you originally paid for it (including any fees). Use a consistent accounting method such as FIFO (First In, First Out), LIFO (Last In, First Out), or specific identification, and apply it across all transactions.

4. File with accurate numbers

Report each crypto disposition on Form 8949 with the correct cost basis. For the 2025 tax year, the IRS introduced new checkbox groups specifically for digital assets. Short-term crypto transactions use Boxes G, H, or I. Long-term crypto transactions use Boxes J, K, or L. If your 1099-DA shows proceeds but the basis field is blank (which is normal for 2025, since brokers aren't required to report basis yet), you'll check Box H for short-term transactions or Box K for long-term transactions. Do not use Box C for crypto. Box C is for non-digital-asset transactions that weren't reported on any broker form. For a full walkthrough with a worked example, see how to fill out Form 8949 for crypto with a real example.

If your 1099-DA shows different numbers than what you calculate, you can report adjustments. The IRS expects discrepancies when cost basis is missing from the 1099-DA, but you need documentation to support your figures.

For a complete step-by-step walkthrough of filling out Form 8949 and Schedule D, see our crypto tax filing guide.

Don't let missing cost basis cost you money

Cryptofolio reconstructs your complete transaction history across wallets, exchanges, and DeFi protocols, so your cost basis is accurate when you need it.

How Cryptofolio Helps

Manually reconstructing cost basis across multiple exchanges and wallets is tedious and error-prone. Cryptofolio automates the process:

- Connects all your exchanges and wallets in one dashboard with read-only API connections. No custody, no risk.

- Automatically matches transfers between platforms using transaction binding, so your cost basis follows your assets wherever they go.

- Tracks all DeFi transaction types, including staking rewards, bridge transfers between chains, airdrop claims, token swaps on DEXs, and liquidity pool entries and exits. These are the complex transactions that exchanges can't track and 1099-DAs don't cover.

- Generates tax-ready reports with accurate cost basis for every disposition, ready to send to your accountant or tax platform.

Instead of spending hours in spreadsheets trying to trace a single ETH transfer across three platforms, Cryptofolio does it automatically. For a deeper dive into how cost basis works and how to calculate it, see our crypto cost basis guide. For a complete overview of what a portfolio tracker tracks and how it differs from balance trackers and tax software, see our portfolio tracker guide. For a comparison of how different tools handle the cost basis gap, see our Koinly vs CoinTracker vs Cryptofolio guide.

What Changes in 2027?

The rules are getting stricter. Starting with tax year 2026 (filed in 2027), brokers will be required to report cost basis for assets acquired on or after January 1, 2026. This means:

- Exchanges will track cost basis from the moment you buy on their platform.

- Transfers between brokers will eventually be covered by a new "transfer statement" system, similar to how stock brokerages transfer cost basis today.

- DeFi and self-custodied wallets remain a gray area. The IRS is still developing rules for decentralized platforms.

But for the 2025 tax year you're filing now, you're largely on your own for cost basis. That's why getting organized today matters.

For context on the broader regulatory framework, including the SEC's March 2026 interpretation on how crypto assets are classified, see our SEC crypto taxonomy overview.

What Happens If You Get It Wrong?

Ignoring missing cost basis, or just accepting the 1099-DA numbers without adjustments, can lead to serious consequences:

- Overpaying taxes. If you don't report your cost basis, the IRS treats your basis as zero. You could end up paying capital gains tax on money you never actually made.

- IRS notices. If your Form 8949 doesn't match what exchanges report on 1099-DAs, expect a CP2000 notice from the IRS asking for an explanation. For the full list of mistakes that trigger IRS notices and how to avoid them, see our tax mistakes guide.

- Penalties and interest. Underreporting income, even unintentionally, can trigger accuracy-related penalties of 20% on top of the tax owed, plus interest.

- Audit risk. Significant discrepancies between reported income and 1099-DA data can flag your return for a closer look.

The safest approach is to proactively report accurate cost basis, even if your 1099-DA doesn't include it. The IRS has stated they expect taxpayers to maintain their own records.

The Bottom Line

Form 1099-DA is here, and it's not going away. For the 2025 tax year, millions of crypto users are receiving this form for the first time, and many are discovering that their cost basis is missing.

That's not a reason to panic, but it is a reason to act. If you don't report accurate cost basis, you could end up overpaying the IRS by thousands of dollars, or worse, facing penalties for underreporting.

The solution is straightforward: gather your transaction history, match transfers across platforms, and calculate your actual cost basis. Tools like Cryptofolio can automate this process, saving you hours of manual work and reducing the risk of errors.

Don't wait until the filing deadline. Start organizing your crypto tax records now.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. While we strive to keep our content accurate and up to date, information in this article may become outdated as policies evolve. Consult a qualified tax professional for advice on your individual circumstances.