How to File Crypto Taxes Step by Step: Form 8949, Schedule D, and Your 2025 Return

A step-by-step walkthrough of filing your 2025 crypto taxes. Covers Form 1099-DA, Form 8949, Schedule D, and Form 1040, including the new digital asset checkboxes.

The IRS deadline is April 15. If you sold, swapped, spent, or otherwise disposed of crypto in 2025, those transactions need to appear on your tax return. For most people, that means filling out Form 8949, carrying the totals to Schedule D, and reporting the final number on Form 1040.

This guide walks through every step in order, from gathering your 1099-DA to choosing the right checkbox on Form 8949 to getting the numbers onto your 1040. It also covers the new digital asset checkbox groups that apply for the first time this year.

What Forms Do You Need?

Filing crypto taxes involves four forms, each building on the previous one.

Form 1099-DA is the new IRS information return that centralized exchanges are required to send you for the 2025 tax year. It reports your gross proceeds from each digital asset disposal. Think of it as the source document, not the final answer. For most filers, it will show proceeds but not cost basis. (For a full breakdown of what 1099-DA reports and what it leaves out, see our 1099-DA explainer.)

Form 8949 is where you report each individual crypto disposal. You list the asset, acquisition date, sale date, proceeds, cost basis, and resulting gain or loss. Every taxable disposal goes here, including sales, swaps, DeFi transactions, and crypto used to pay fees. For a column-by-column walkthrough with a real worked example, see how to fill out Form 8949 for crypto.

Schedule D is the summary form. You transfer the totals from Form 8949 to Schedule D, which separates your transactions into short-term (held 1 year or less) and long-term (held over 1 year) and calculates your net capital gain or loss.

Form 1040 is your main tax return. The net capital gain or loss from Schedule D flows to line 7 of Form 1040. The digital asset question on line 7a of Schedule 1 also asks whether you received, sold, exchanged, or otherwise disposed of a digital asset during the year. If you had any crypto activity, you answer yes.

Step 1: Gather Your 1099-DA and Complete Transaction List

Your 1099-DA from each exchange is your starting point, but it is not your complete picture. Exchanges are required to report proceeds from on-exchange sales. They cannot report transactions that happened elsewhere: wallet-to-wallet transfers, DeFi activity, staking rewards, airdrops, or anything that originated off their platform.

Before you open Form 8949, you need a complete list of every disposal you made in 2025. This includes sales on centralized exchanges (covered by your 1099-DA), crypto-to-crypto swaps on DEXs, tokens spent on gas fees, LP deposits and withdrawals, and staking reward sales. Each of these is a separate line on Form 8949.

For each disposal, you need four pieces of data: the asset description, the date you acquired it, the date you disposed of it, and the cost basis. The proceeds will come from your 1099-DA for exchange transactions, or from your own records for everything else.

(For a detailed walkthrough of how to reconstruct complete cost basis across exchanges and wallets, see our cost basis guide.) For more on how transfers affect your cost basis specifically, see our transfer guide.

Step 2: Separate Short-Term and Long-Term Disposals

Form 8949 has two parts: Part I for short-term disposals (assets held 1 year or less) and Part II for long-term disposals (assets held more than 1 year). Before you start filling in columns, go through your disposal list and sort each transaction by holding period.

The holding period starts the day after you acquired the asset and ends on the day you disposed of it. If you bought Bitcoin on March 5, 2024, and sold it on March 5, 2025, that is exactly one year and counts as short-term. One more day (March 6, 2025) would make it long-term.

This matters because short-term gains are taxed at your ordinary income rate (up to 37%) while long-term gains are taxed at preferential rates (0%, 15%, or 20% depending on your income). Sorting by holding period is not optional; it determines which part of the form you use and which tax rate applies.

Step 3: Choose the Right Checkbox

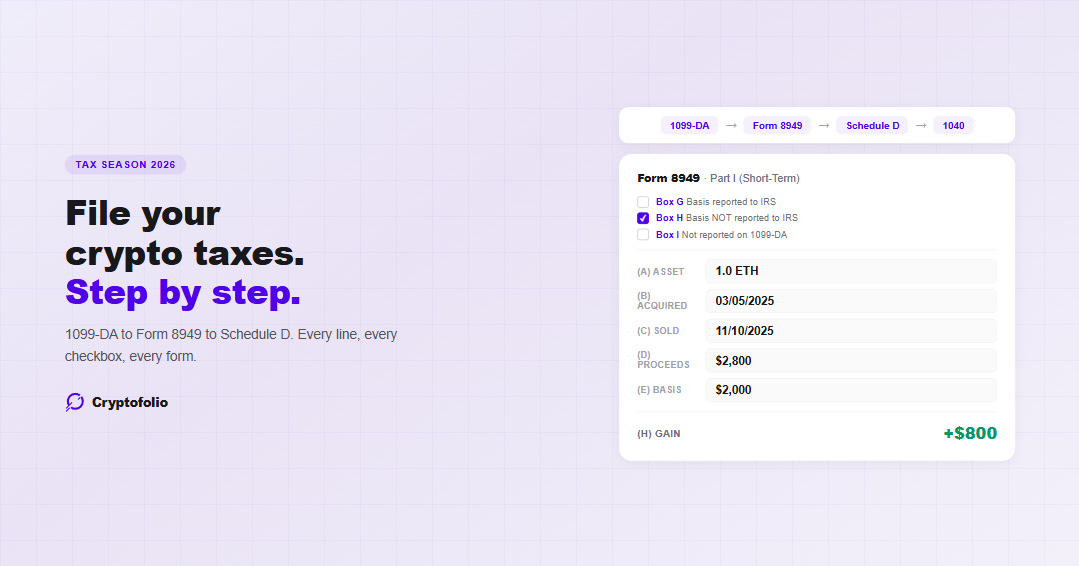

Each part of Form 8949 has three checkbox options. For 2025, the IRS added new checkbox groups specifically for digital assets reported on Form 1099-DA. You must check exactly one box per part, and the box you check determines which line of Schedule D receives the totals.

Short-term checkboxes (Part I):

Long-term checkboxes (Part II):

Most crypto investors filing for the 2025 tax year will check Box H (short-term) and Box K (long-term). For 2025, brokers are required to report proceeds but not cost basis on Form 1099-DA. This means your 1099-DA will show proceeds but the basis field will be blank or marked with Code Y, which means basis was not reported to the IRS. Box H and Box K are for exactly this situation.

If you also have transactions not covered by any 1099-DA (DeFi, self-custody, staking rewards), you will need additional pages: one for Box H/K and one for Box I/L.

Do not use Box C or Box F for crypto transactions. Those boxes are for stocks, bonds, and other traditional securities. Crypto uses the new digital asset boxes (G, H, I for short-term and J, K, L for long-term). Using the wrong box will create a mismatch with what your exchange reported on Form 1099-DA.

Step 4: Fill In the Columns

Each row on Form 8949 represents one disposal. Here is what goes in each column:

Example: What a Completed Form 8949 Row Looks Like

You bought 1.0 ETH on March 5, 2025 for $2,000. You sold it on November 10, 2025 for $2,800. Your exchange sent you a 1099-DA showing $2,800 in proceeds but no cost basis (Code Y). You check Box H (short-term, basis not reported).

Step 5: Transfer Totals to Schedule D

Once you have filled out all your Form 8949 rows, total up column (d) (proceeds), column (e) (basis), and column (h) (gain or loss) for each checkbox group. Then transfer those totals to the corresponding line on Schedule D.

Short-term (Part I of Schedule D):

Long-term (Part II of Schedule D):

Schedule D then combines the short-term net (line 7) and long-term net (line 15) to produce your overall net capital gain or loss on line 16. If line 16 is a net loss, you can deduct up to $3,000 against ordinary income. Any excess loss carries forward to future years.

Step 6: Report on Form 1040

The net capital gain or loss from Schedule D, line 16 flows to Form 1040, line 7. This adds to (or reduces) your total taxable income for the year.

Separately, you must answer the digital asset question on Schedule 1, line 8z (formerly on Form 1040 directly). The question asks whether you received, sold, exchanged, gifted, or otherwise disposed of a digital asset during 2025. Answer yes if you had any disposals. Answer yes even if your overall gain was zero or you had a net loss.

Filing Checklist

Before you submit, work through this checklist:

For a deeper look at the mistakes that trigger IRS notices and how to avoid them, see our tax mistakes guide.

How Cryptofolio Handles This

The hard part of filing crypto taxes is not the forms themselves. It is having accurate, complete data before you start. Every Form 8949 line requires a cost basis number. For most people, that number is missing, wrong, or fragmented across exchanges, wallets, and DeFi protocols.

Cryptofolio connects to all your exchanges and wallets, matches transfers automatically, and maintains wallet-level FIFO lot queues across your entire portfolio. When you are ready to file, the gain/loss numbers for every disposal are already calculated and organized by the correct Form 8949 checkbox group.

You can also see your tax position before you sell, which lets you make informed decisions about timing and lot selection rather than discovering the tax impact after the fact. For more on how lot selection affects your tax bill, see our FIFO vs. LIFO vs. Specific Identification guide.

Start with accurate data. File with confidence.

Cryptofolio maintains lot-level cost basis across all your wallets and exchanges, so your Form 8949 numbers are ready when you need them.

The Bottom Line

Filing crypto taxes in 2026 means working through four forms in order: 1099-DA, Form 8949, Schedule D, and Form 1040. The new digital asset checkbox groups (G through L) replace the old stock/bond boxes for crypto transactions.

Most filers will use Box H (short-term) and Box K (long-term) because their 1099-DA shows proceeds but not cost basis. You will need to supply the cost basis yourself, line by line, from your own records. For DeFi and self-custody activity with no 1099-DA at all, use Box I and Box L.

The forms are straightforward once you have the data. Getting the data right is the work.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. While we strive to keep our content accurate and up to date, information in this article may become outdated as policies evolve. Consult a qualified tax professional for advice on your individual circumstances.