FIFO vs LIFO vs Specific Identification: Choosing the Right Crypto Tax Method

FIFO, LIFO, and Specific Identification can produce dramatically different tax bills on the same crypto transactions. Learn how each method works and which one to use.

You bought Bitcoin three times over the past two years. Now you're selling some. The IRS wants to know: which Bitcoin are you selling?

Your answer to that question determines your tax bill. Depending on the method you choose, you could owe $3,750, $1,200, or nothing at all on the exact same sale. The difference isn't a loophole or a trick. It's a choice the IRS gives you, and most crypto investors either don't know about it or don't understand how to use it.

This guide explains the three accounting methods available for crypto taxes: FIFO, LIFO, and Specific Identification. We'll walk through how each one works, show the tax impact on identical transactions, and help you decide which method makes sense for your situation.

Why the Method Matters

When you sell crypto, you need to determine the cost basis of the units you're selling. If you bought Bitcoin once and sold all of it, this is simple. But if you bought the same asset multiple times at different prices, you have multiple "lots," and the IRS needs to know which lot you're selling.

Your cost basis method determines which lot gets matched to the sale. Different lots have different purchase prices and different holding periods, which means different tax outcomes.

(For a full explanation of cost basis and how it works across wallets and exchanges, see our cost basis guide.)

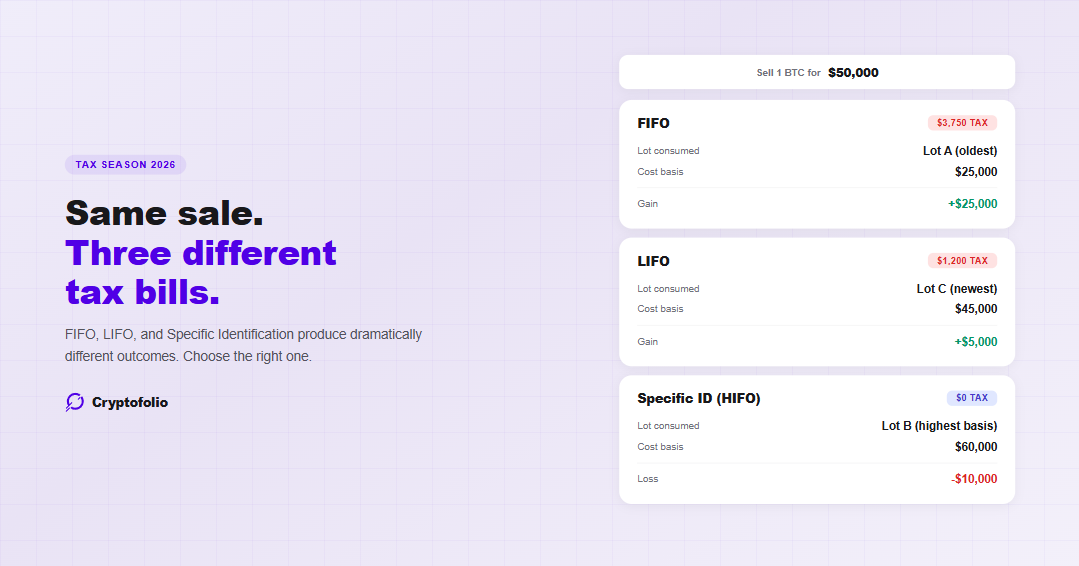

The Same Sale, Three Different Tax Bills

Let's use a concrete example. You made three Bitcoin purchases over time:

Your lots:

- Lot A: 1 BTC bought January 2024 for $25,000

- Lot B: 1 BTC bought August 2024 for $60,000

- Lot C: 1 BTC bought January 2025 for $45,000

The sale: You sell 1 BTC in March 2026 for $50,000.

Here's what happens under each method:

Sells the oldest lot first. Consumes Lot A.

Over 1 year (long-term). Tax at 15%: $3,750

Sells the newest lot first. Consumes Lot C.

Under 1 year (short-term). Tax at 24%: $1,200

You select the lot with the highest basis. Consumes Lot B.

Tax: $0 (plus a $10,000 capital loss to offset other gains)

Same sale. Same proceeds. Three completely different outcomes.

FIFO: First In, First Out

FIFO is the default method under IRS rules. If you don't actively choose a different method, the IRS assumes you're using FIFO. It means you always sell your oldest units first.

How it works: When you dispose of any crypto (sell, swap, spend, pay gas), FIFO looks at your lot queue for that asset in that wallet and consumes the oldest lot first. If the disposal is larger than the oldest lot, it continues to the next oldest lot until the full quantity is covered.

Advantages:

- Simplest to implement. No decisions to make per transaction.

- The IRS default, so there's no additional recordkeeping burden to justify your method.

- Often results in long-term capital gains (since oldest lots have the longest holding periods), which are taxed at lower rates (0%, 15%, or 20% depending on income).

Disadvantages:

- In a market that has gone up over time, your oldest lots have the lowest cost basis. This means FIFO produces the largest gains.

- You have no flexibility. You can't choose a higher-basis lot to reduce your gain.

- In a rising market, FIFO consistently produces the highest tax bills among the three methods.

When FIFO makes sense: If your earliest purchases were at relatively high prices (you bought near a peak and the market dropped), FIFO naturally assigns high-basis lots to your sales, resulting in smaller gains. FIFO also works well if you primarily want long-term capital gains treatment and your portfolio has appreciated steadily.

LIFO: Last In, First Out

LIFO is the opposite of FIFO. You sell your most recently acquired units first.

How it works: When you dispose of crypto, LIFO looks at your lot queue and consumes the newest lot first. If the disposal is larger than the newest lot, it continues to the next most recent lot.

Under the current IRS framework, there are only two permitted methods: FIFO (the default) and Specific Identification. LIFO is not a standalone method. It's implemented as a form of Specific Identification where you consistently identify the most recently acquired units as the ones being sold. You need to meet the Specific Identification requirements (covered below) to use LIFO. The same applies to HIFO.

Advantages:

- In a rising market, your most recent purchases typically have the highest cost basis, which means smaller gains or even losses.

- Can significantly reduce your current-year tax liability compared to FIFO.

Disadvantages:

- Typically produces short-term gains (since the most recent lots have the shortest holding periods), which are taxed at your ordinary income rate. This rate is higher than the long-term capital gains rate.

- Requires you to meet IRS Specific Identification requirements (recordkeeping and, after 2025, communication to your broker).

- If you bought recently at a market low, LIFO assigns those low-basis lots to your sale, creating larger gains.

When LIFO makes sense: When the market has risen significantly and your most recent purchase was near the current price. The high basis reduces the gain, and even though it's short-term, the total tax can still be less than a large long-term gain under FIFO.

Specific Identification: Maximum Control

Specific Identification gives you the most flexibility. You choose exactly which lot to sell for each transaction.

How it works: Before or at the time of each sale, you identify the specific units being sold. This could be the highest-basis lot (to minimize gains), a long-term lot (to get the lower tax rate), or a lot that produces a loss (for tax-loss harvesting).

HIFO (Highest In, First Out) is a popular strategy within Specific Identification. You always select the lot with the highest cost basis, minimizing your taxable gain on every sale. This generally produces the lowest tax bill in most scenarios.

Advantages:

- Maximum tax optimization. You can minimize gains, maximize losses, or choose long-term vs. short-term treatment on a per-transaction basis.

- Enables tax-loss harvesting by specifically selecting lots that are at a loss.

- Over a multi-year period, strategic lot selection can significantly reduce your total tax paid.

Disadvantages:

- Requires meticulous recordkeeping. You must be able to identify every lot and its cost basis at the time of each sale.

- Under IRS rules, you must identify the specific units before or at the time of the sale. You can't retroactively choose lots after the fact.

- After the 2025 temporary relief period (Notice 2025-7) ends, you'll need to communicate your specific identification to your custodial broker before the sale. During 2025, you can record it in your own books and records instead.

IRS Requirements for Specific Identification

The IRS has specific rules about what constitutes a valid specific identification:

Starting in 2026, you must communicate your specific identification to your broker no later than the date and time of the sale. The identification must include enough information to determine which units are being sold, such as the acquisition date and purchase price.

During 2025, under IRS Notice 2025-7, you have temporary relief. You can record the identification in your own books and records (including through standing orders like "always sell highest basis first") without communicating it to your broker. This relief exists because many brokers don't yet have systems to accept these instructions.

You can adopt a standing rule in your books and records that identifies which units are selected for sale. The rule must be established before the sale occurs and must include sufficient information to identify the specific units.

You can set a blanket rule like "always use HIFO" or "always use LIFO" and record it in your books. This counts as specific identification for every transaction that follows that rule, as long as it's documented before the transactions occur.

Side-by-Side Comparison

Here's how the three methods compare across key factors:

| Factor | FIFO | LIFO | Specific ID |

|---|---|---|---|

| Tax optimization | None | Limited | Full control |

| Recordkeeping | Lowest | Moderate | Highest |

| Default method? | Yes | No | No |

| Rising markets | Worst | Good | Best |

| Falling markets | Good | Worst | Best |

| Holding period | Long-term | Short-term | Your choice |

The Wallet-by-Wallet Rule Changes Everything

Starting January 1, 2025, the IRS requires cost basis tracking on a wallet-by-wallet and account-by-account basis under Revenue Procedure 2024-28. This directly affects how your accounting method works.

What this means for FIFO: If you sell Bitcoin from your Kraken account, FIFO only consumes lots held in your Kraken account. Even if you have older, lower-basis Bitcoin sitting in a Coinbase account, those lots are not in scope. Each wallet and exchange account has its own independent FIFO queue.

What this means for Specific Identification: You can only specifically identify lots within the wallet or account where the sale occurs. You can't reach into a different wallet to select a lot with better tax treatment.

What this means for your strategy: The location of your lots matters as much as the method you choose. If your highest-basis Bitcoin is in a Ledger wallet but you're selling from Coinbase, Specific Identification can only select from Coinbase's lot queue. This means strategic transfers between wallets before selling can be an important part of tax planning (transfers between your own wallets are not taxable events, but the lots must be moved first).

The safe harbor: If you used a global (universal) FIFO approach before 2025, Revenue Procedure 2024-28 provides a safe harbor for reallocating your pre-2025 cost basis across your wallets as of January 1, 2025. This was a one-time transition opportunity. (For more detail on wallet-by-wallet tracking, see our cost basis guide.) Under the rules effective January 1, 2025, these methods now apply only within each wallet, not across your whole portfolio. See the full breakdown of the wallet-by-wallet rules.

Common Scenarios

Scenario 1: You bought Bitcoin steadily over 3 years and want to sell some

Your lots range from $15,000 to $65,000 per BTC. Current price: $50,000.

HIFO saves you $5,250 and gives you a usable capital loss.

Scenario 2: You bought ETH before a crash and want to harvest losses

You bought ETH at $4,000 (Lot A, January 2025) and $1,800 (Lot B, August 2025). Current price: $2,200. You sell 1 ETH.

Here FIFO and Specific ID produce the same result, but LIFO would be the worst choice.

Scenario 3: DeFi activity with dozens of small transactions

You've been swapping tokens on DEXs, paying gas fees, and claiming staking rewards. Each of these is a disposal that triggers a cost basis calculation.

For high-frequency activity, FIFO is usually the most practical choice. Trying to specifically identify lots on every $5 gas fee payment is impractical. Many DeFi-active users set a standing HIFO order for all transactions, which automates the selection while still qualifying as Specific Identification.

(For more on how DeFi transactions are taxed, see our DeFi tax guide. For a detailed look at how trading bots create lot-level tracking nightmares at even higher volumes, see our trading bot tax guide.)

Important Rules to Know

Consistency matters. For a given wallet or account, you must use the same method for the entire tax year. You cannot switch methods mid-year within the same wallet. However, different wallets or accounts may use different methods. You can also change your method from one tax year to another without IRS approval.

You can't change retroactively. Once you've filed a tax return using a particular method, you generally can't go back and recalculate using a different method for that year. Choose carefully before filing. For a full walkthrough of how to report your disposals on Form 8949 and Schedule D, see our crypto tax filing guide.

The wash sale rule currently does not apply to crypto. As of 2026, the wash sale rule (which prevents you from selling a stock at a loss and immediately rebuying it) does not apply to cryptocurrency. This means you can sell crypto at a loss to harvest the tax benefit and immediately repurchase the same asset. This could change if Congress extends Section 1091 to digital assets in the future, but for now, crypto investors can take advantage of this. For a complete guide to using your losses strategically, see our tax-loss harvesting guide.

Short-term vs. long-term rates matter. Short-term capital gains (assets held 1 year or less) are taxed at your ordinary income rate, which can be as high as 37%. Long-term capital gains (held over 1 year) are taxed at 0%, 15%, or 20% depending on your income. Sometimes a smaller long-term gain under FIFO results in less tax than a larger short-term loss offset under LIFO. Run the numbers both ways.

How Cryptofolio Handles This

Choosing the right method and applying it correctly across hundreds or thousands of transactions is where most people get stuck. Each disposal needs to pull from the correct lot in the correct wallet's queue using the correct method.

Cryptofolio maintains per-wallet FIFO queues for every asset across all your connected exchanges and wallets. When you sell, the system applies your chosen method automatically and correctly, whether that's FIFO, LIFO, or HIFO via Specific Identification.

Because Cryptofolio tracks lot-level data in real time (not reconstructed at tax time), you can see the tax impact of different methods before you sell. This lets you make informed decisions about which lots to dispose of and from which wallet, rather than discovering the tax consequences after the fact.

Pick the right method. Apply it automatically.

Cryptofolio maintains per-wallet FIFO queues and lets you choose your accounting method across all connected exchanges and wallets.

The Bottom Line

The accounting method you choose is one of the few areas where you have genuine control over your crypto tax outcome. FIFO is the safe default, but it's rarely the optimal choice. Specific Identification (particularly HIFO) gives you the most flexibility to minimize taxes legally.

The key requirements are accurate lot-level recordkeeping and, starting in 2026 for broker-custodied assets, communicating your method choice to your broker. During 2025, the temporary relief under Notice 2025-7 gives you time to set up standing orders in your own records.

Whatever method you choose, apply it consistently and document it. The IRS doesn't require you to pay the most tax possible. They require you to pick a method, follow it, and keep records that prove it.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. While we strive to keep our content accurate and up to date, information in this article may become outdated as policies evolve. Consult a qualified tax professional for advice on your individual circumstances.