Crypto Tax-Loss Harvesting: How to Turn Losses Into Tax Savings

Crypto losses can offset capital gains and reduce your taxable income by up to $3,000 per year. Learn how tax-loss harvesting works, why crypto has a unique advantage over stocks, and how to do it right.

You bought Bitcoin at $60,000. Right now, it's worth $42,000. You're sitting on an $18,000 unrealized loss. That loss is doing nothing for you.

But if you sell that Bitcoin today, you turn an unrealized loss into a realized loss. That $18,000 capital loss can now offset capital gains from other investments. If your total losses exceed your total gains, you can deduct up to $3,000 from your ordinary income this year. Whatever is left carries forward to future tax years, indefinitely.

And here's the part that makes crypto different from stocks: you can buy the Bitcoin right back. Today. There's no waiting period.

This is crypto tax-loss harvesting, and it's one of the most effective legal strategies available to reduce your tax bill.

How It Works

Tax-loss harvesting is the process of selling an investment at a loss to create a capital loss you can use to offset other gains. The loss must be realized, meaning you actually sell, swap, or otherwise dispose of the asset. Paper losses from holding an asset that dropped in value don't count.

Once realized, your capital losses can offset capital gains from any source. Crypto losses can offset crypto gains, stock gains, real estate gains, or any other capital gains. There is no limit on how much you can offset. If you have $50,000 in capital losses and $50,000 in capital gains, they cancel out completely.

If your losses exceed your gains, you can deduct up to $3,000 of the excess against your ordinary income ($1,500 if married filing separately). Any remaining losses carry forward to future tax years with no expiration. You keep using them until they are fully exhausted. Crypto losses aren't limited to offsetting crypto gains. See how crypto losses can cancel stock gains dollar for dollar.

(For a full explanation of how capital gains and losses flow through your tax return, see our filing guide.)

The Crypto Advantage: No Wash Sale Rule

With stocks, there's a catch. The IRS wash sale rule (IRC §1091) says that if you sell a stock or security at a loss and buy a "substantially identical" stock or security within 30 days before or after the sale, the loss is disallowed. You can't claim it.

This rule does not apply to cryptocurrency.

IRC §1091 explicitly applies only to "stock or securities." The IRS classifies crypto as property, not a security. Because crypto falls outside that definition, you can sell Bitcoin at a loss, claim the full loss on your taxes, and buy it back the next minute. There is no 30-day waiting period.

This makes crypto tax-loss harvesting significantly more powerful than the stock equivalent. With stocks, you either wait 30 days (risking a price rebound) or swap into a similar but not identical asset. With crypto, you can maintain your exact position while still capturing the tax benefit.

The SEC's March 2026 interpretation formally classifying most crypto assets as digital commodities rather than securities further reinforces this position. See our SEC taxonomy overview for the full breakdown.

Bitcoin and Ethereum ETFs (like GBTC, ETHE, and spot Bitcoin ETFs) are classified as securities, not property. The wash sale rule does apply to these products. If you sell a Bitcoin ETF at a loss and repurchase it within 30 days, the loss is disallowed. This only applies to the ETF shares, not to holding Bitcoin directly.

Will this change? Possibly. Congress has discussed extending the wash sale rule to digital assets in multiple legislative proposals, including provisions in the PARITY Act. As of March 2026, no such legislation has been enacted. The wash sale rule still does not apply to direct crypto holdings. But this window may not remain open indefinitely.

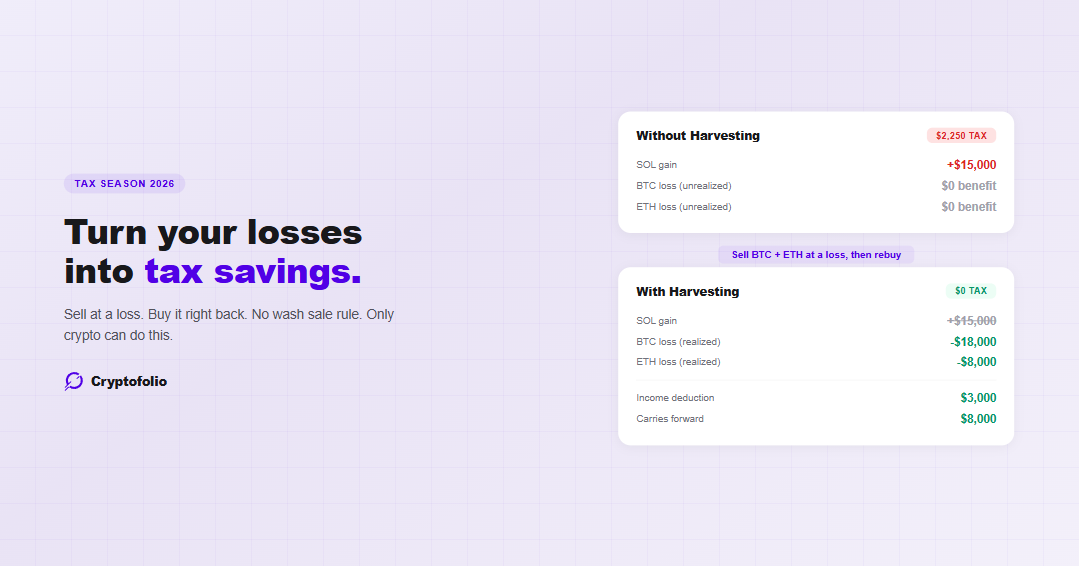

A Worked Example

You made several investments during 2025:

- Bought 1 BTC for $60,000 (now worth $42,000, unrealized loss of $18,000)

- Bought 5 ETH for $20,000 total (now worth $12,000, unrealized loss of $8,000)

- Sold SOL during the year for a $15,000 capital gain

Instead of paying $2,250 on the SOL gain, you pay $0 on capital gains and save an additional amount on the $3,000 ordinary income deduction. If you're in the 24% income tax bracket, that's another $720 in savings.

Your repurchased BTC and ETH now have a new, lower cost basis ($42,000 for BTC and $12,000 for ETH). If the market recovers, you will owe more in the future when you sell because your basis is lower. You are not eliminating the tax. You are deferring it, and you are getting the cash benefit today.

The Netting Rules

The IRS has specific rules for how capital gains and losses are combined. Understanding these matters because short-term and long-term gains are taxed at different rates.

Why this matters for harvesting: Short-term gains are taxed at your ordinary income rate (up to 37%). Long-term gains are taxed at preferential rates (0%, 15%, or 20%). A short-term loss that offsets a short-term gain saves you more per dollar than a long-term loss offsetting a long-term gain. When choosing which positions to harvest, consider both the size of the loss and whether it will offset short-term or long-term gains.

What Resets When You Repurchase

Selling and rebuying is not a free lunch. Two things change when you repurchase:

This is the tradeoff. You get a real tax benefit today. But if the asset recovers, your future tax bill will be higher, and your future gains may be taxed at higher short-term rates until you cross the one-year holding threshold again.

For most investors, the math still works. Getting a tax deduction today is more valuable than a potentially larger gain years from now. But run the numbers for your specific situation.

How to Choose Which Losses to Harvest

Not all losses are equally valuable to harvest. Here's how to prioritize:

Largest losses first. The bigger the gap between your cost basis and current market value, the more tax benefit you capture by harvesting.

Short-term losses over long-term losses (when offsetting short-term gains). A short-term loss that offsets a short-term gain saves you tax at your ordinary income rate (up to 37%). A long-term loss that offsets a long-term gain saves you tax at the lower capital gains rate (up to 20%).

Losses from assets you want to keep holding. Since you can immediately repurchase in crypto, you don't need to give up positions you believe in. Harvest the loss and maintain the same exposure.

Losses across multiple wallets. Under the wallet-by-wallet rule, each wallet has its own lot queue. You may have unrealized losses in one wallet and gains in another. Review every wallet.

Your accounting method determines which lots get sold first. If you're using FIFO, the oldest lots are consumed first, which may not be the lots with the largest losses. Specific Identification (HIFO) lets you target the lots with the highest cost basis, which are often the ones with the biggest unrealized losses. This makes Specific Identification the most effective method for tax-loss harvesting.

(For a full comparison of FIFO, LIFO, and Specific Identification, see our accounting methods guide.)

When to Harvest

Before December 31. Losses must be realized within the calendar year to count on that year's tax return. If you wait until January 1, the loss applies to next year instead.

During market dips throughout the year. You don't have to wait until December. If the market drops 30% in June, you can harvest then and still have the rest of the year to capture additional losses if the market drops further.

Before selling winners. If you're planning to sell a profitable position later in the year, harvest your losses first. The realized losses will be ready to offset the gains when you take them.

Don't wait until the last minute. Exchange delays, network congestion, and settlement times can prevent a sale from being recorded before midnight on December 31. Give yourself a buffer of at least a few days.

Common Mistakes

Harvesting losses you can't document. Every harvested loss needs a clear cost basis and transaction record. If you can't prove your original purchase price, the IRS can treat your basis as zero, which means you might not have a loss at all. If you have transferred crypto between wallets and lost track of the original cost basis, fix your records before harvesting. For a complete look at the filing mistakes that lead to IRS notices, see our crypto tax mistakes guide.

Forgetting that the holding period resets. If you harvest a long-term position and repurchase, you are now back to short-term. If the price rises quickly and you sell again within a year, you will pay the higher short-term rate on the new gain.

Selling to a related party. The IRS may disallow losses on sales between related parties (spouses, entities you control). Make sure your sale is a real market transaction.

Not tracking repurchase basis. When you repurchase, your new cost basis is the repurchase price. If you don't record this, you will have the same cost basis problem later that you would have had without harvesting.

Assuming it works for crypto ETFs. Bitcoin and Ethereum ETFs are securities. The wash sale rule applies to them. Selling a Bitcoin ETF at a loss and rebuying within 30 days disallows the loss. This only applies to the ETF, not to holding BTC directly.

Harvesting tiny losses at high transaction cost. If the gas fee or exchange fee to execute the harvest exceeds the tax savings, the trade isn't worth it. Gas fees are taxable dispositions themselves, which adds another layer to the calculation.

How to Report Harvested Losses

Harvested losses are reported on your tax return like any other capital loss.

Each sale goes on Form 8949 with the date acquired, date sold, proceeds, cost basis, and gain or loss. The loss flows through to Schedule D, where it is combined with your other capital gains and losses. Harvested losses get reported on Form 8949 before flowing to Schedule D. See the full worked example.

If you repurchased the same asset, the repurchase is a separate transaction. It establishes a new lot with a new cost basis and a new holding period start date. The repurchase itself is not reported until you eventually sell again.

Make sure the proceeds on your Form 8949 match what your exchange reported on Form 1099-DA. The IRS will cross-reference these.

How Cryptofolio Helps

The hardest part of tax-loss harvesting is knowing which positions have unrealized losses, how large those losses are, and which lots to target. If your crypto is spread across multiple exchanges and wallets, each with different cost basis data, identifying harvest opportunities manually is nearly impossible.

Cryptofolio tracks your cost basis in real time across every connected wallet and exchange. You can see your unrealized gains and losses at any time, broken down by lot, by wallet, and by asset. When a harvesting opportunity appears, you already know the exact cost basis, the lot selection under your chosen accounting method, and the tax impact of the sale before you execute it.

This is the difference between guessing and knowing. And when the difference can be thousands of dollars in tax savings, knowing matters.

See your unrealized losses in real time.

Cryptofolio tracks your cost basis across every wallet and exchange, so you always know which positions have harvestable losses and how much they're worth.

The Bottom Line

If you are holding crypto that is worth less than what you paid, you have a tax asset sitting in your portfolio. Every day you don't harvest that loss is a day the tax benefit sits unused.

The current exemption from the wash sale rule gives crypto investors an advantage that stock investors don't have. You can realize the loss, claim the tax benefit, and maintain your position. This window may not last forever.

The mechanics are straightforward: sell, claim the loss, repurchase if you want to. The complexity is in knowing your cost basis, choosing the right lots, and tracking everything correctly across wallets and exchanges. Get those right, and tax-loss harvesting becomes one of the most powerful tools in your portfolio.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. While we strive to keep our content accurate and up to date, information in this article may become outdated as policies evolve. Consult a qualified tax professional for advice on your individual circumstances.