Crypto Tax Mistakes That Trigger IRS Notices (And How to Avoid Them)

The IRS is matching your 1099-DA against your tax return. These are the crypto tax mistakes that trigger CP2000 notices, accuracy penalties, and audits, and how to avoid them.

This is the first year the IRS has direct visibility into your crypto transactions. Every centralized exchange that processed a sale, swap, or disposal for you in 2025 sent a Form 1099-DA to both you and the IRS. That form reports the proceeds from each transaction.

The IRS feeds that data into its Automated Underreporter (AUR) system. The AUR compares the proceeds your exchange reported against what you reported on your tax return. If there is a mismatch, the system generates a CP2000 notice proposing additional taxes, plus interest and potentially penalties.

A CP2000 is not an audit. It is an automated letter that says: "We received information showing income you may not have reported. Here is what we think you owe." You typically have 30 days from the date on the notice to respond. If you do not respond, the IRS moves forward with the proposed amount.

In 2021, the IRS sent thousands of CP2000 notices to crypto holders based on incomplete 1099-K data from exchanges. Many of those notices overstated what was owed because the forms did not account for cost basis. Now, with the 1099-DA reporting gross proceeds to the IRS for the first time, the same pattern is about to happen at a much larger scale.

The good news: most of these notices are triggered by preventable mistakes. Here are the ones that matter most and how to avoid each one.

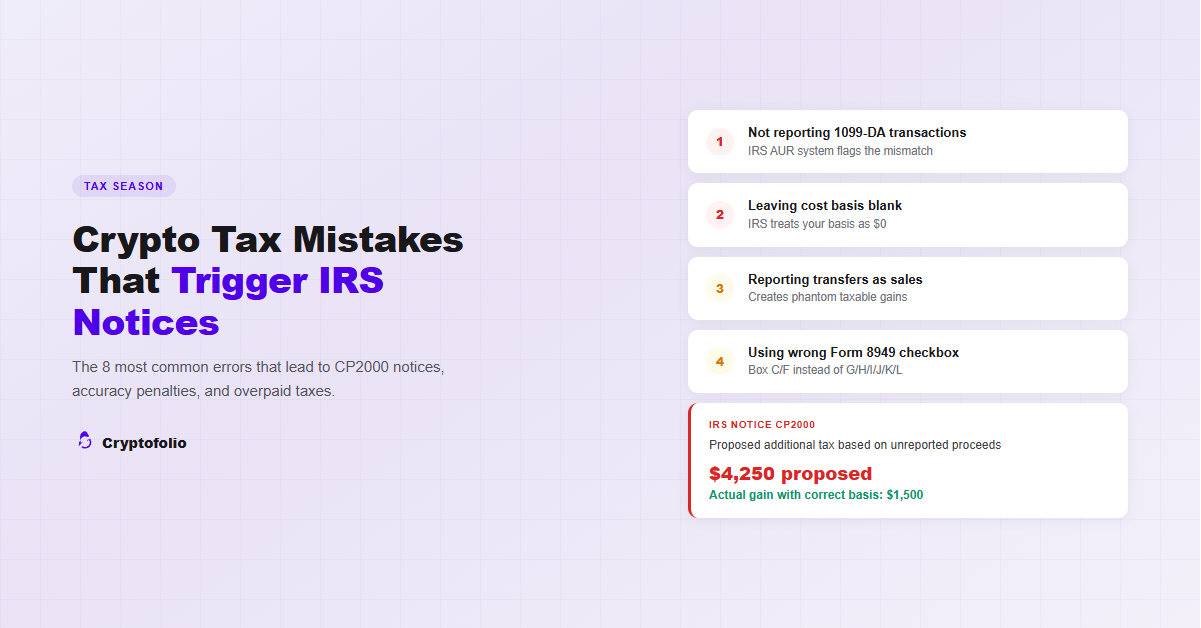

Mistake #1: Not Reporting Transactions That Appear on Your 1099-DA

This is the single most common trigger for a CP2000 notice. Your exchange sent your 1099-DA to the IRS. If you do not report those same transactions on your Form 8949, the AUR system flags the difference.

Some people skip reporting because they think their activity was too small to matter. Others assume that because they lost money overall, they do not need to file. Neither assumption is correct. Every disposal reported on your 1099-DA needs a corresponding entry on your Form 8949, regardless of whether it resulted in a gain or a loss.

If you used multiple exchanges, you received multiple 1099-DAs. Each one must be accounted for. Missing even a single form can trigger a notice.

Before you file, collect every 1099-DA you received. Compare each transaction against your Form 8949. Make sure every disposal your exchange reported has a matching row on the form. For a step-by-step walkthrough of how to fill out Form 8949, see our filing guide.

Mistake #2: Leaving Cost Basis Blank or Reporting It as Zero

For the 2025 tax year, most 1099-DAs report proceeds but not cost basis. If you leave the cost basis column empty on Form 8949, the IRS treats your basis as zero. That means your entire proceeds become taxable gain.

Consider the math. You bought 1 ETH for $2,000 and sold it for $3,500. Your actual gain is $1,500. But if you report $3,500 in proceeds with no cost basis, the IRS sees a $3,500 gain.

Multiply that across dozens of transactions and the overpayment adds up quickly. This mistake also works in the other direction. If you underreport because you guessed at a basis that was too high, the IRS may propose additional tax.

Always supply your own cost basis from your records, even when your 1099-DA leaves the field blank. Check Box H (short-term) or Box K (long-term) on Form 8949 to indicate that your broker reported proceeds but not basis. The IRS expects this for 2025 filings. For how to calculate and reconstruct your cost basis, see our cost basis guide.

Mistake #3: Reporting Transfers as Sales

Moving crypto from Coinbase to MetaMask is not a sale. Moving it from MetaMask to Kraken is not a sale. These are transfers between your own wallets, and they are not taxable events under IRS FAQ A81.

But some people report these on Form 8949 as disposals, creating phantom gains. Others use tax software that misclassifies incoming deposits as new purchases, which resets the cost basis and creates errors when the asset is eventually sold.

The opposite problem also happens. Some people see a large deposit on an exchange and assume it was income. An incoming transfer of your own crypto is not income. It is a movement of an asset you already own.

For each transaction on your record, determine whether it was a disposal (sale, swap, spend, fee payment) or a transfer (movement between your own wallets). Only disposals go on Form 8949. Transfers should be excluded from the form but documented in your records so the cost basis carries through. For a detailed breakdown of how transfers affect your cost basis, see our transfer guide.

Mistake #4: Using the Wrong Checkbox on Form 8949

For the 2025 tax year, Form 8949 has new checkbox groups specifically for digital assets. Boxes G, H, and I cover short-term transactions. Boxes J, K, and L cover long-term. Each box corresponds to a different reporting scenario.

Some filers use Box C or Box F out of habit. Those boxes are for non-digital-asset transactions. If your exchange reported your crypto disposals on a 1099-DA and you filed under Box C, you have created a mismatch. The IRS system expects to see your 1099-DA data under the digital asset boxes. When it does not find a match, it flags your return. The most common error this season is checking Box C for crypto when it should be Box H or Box K. See the full Form 8949 worked example.

Another common error is filing all transactions under one checkbox when you should be using multiple. If you have exchange transactions reported on a 1099-DA and DeFi transactions with no 1099-DA, those require separate Form 8949 pages: one for Box H/K (1099-DA without basis) and one for Box I/L (no 1099-DA at all).

Use the correct digital asset checkboxes. Most people filing for 2025 will use Box H (short-term, basis not reported) and Box K (long-term, basis not reported). For DeFi and self-custody disposals with no 1099-DA, use Box I and Box L. Never use Box C or Box F for crypto. For the full checkbox breakdown, see our filing guide.

Mistake #5: Ignoring DeFi, Staking, and Airdrop Income

Your 1099-DA only covers transactions on centralized exchanges. Under IRS Notice 2024-57, most DeFi transactions are temporarily excluded from broker reporting. That includes DEX swaps, liquidity pool activity, staking rewards, lending, and wrapping.

The exclusion from reporting does not mean these transactions are tax-free. Every DEX swap is a taxable disposal. Every staking reward is ordinary income at fair market value when you gain dominion and control. Every airdrop you claimed is income. Even the gas fees you paid to execute these transactions are dispositions that run through your lot queue.

Many people file only the transactions that appear on their 1099-DA and ignore everything else. The IRS may not catch this immediately through AUR matching, since no 1099-DA was issued for the DeFi activity. But the IRS has access to blockchain analytics tools and can see on-chain activity. If a later review or audit reveals unreported DeFi income, the consequences are more severe than a CP2000 notice, because the underreporting was on transactions with no information return, which makes it harder to claim good faith.

Report all taxable crypto activity on your return, not just what appears on your 1099-DA. Pull your on-chain transaction history from every wallet you used. Classify each interaction: swaps, staking rewards, airdrop claims, LP entries and exits, gas fees. Each of these needs to be reported. For a complete breakdown of how each DeFi transaction type is taxed, see our DeFi tax guide. For a detailed breakdown of how airdrops specifically are taxed, including the cost basis trap and double-taxation, see our airdrop tax guide.

Mistake #6: Using a Global FIFO Instead of Wallet-by-Wallet

Before 2025, many taxpayers and tax software tools calculated FIFO across their entire portfolio as a single pool. Starting January 1, 2025, the IRS requires cost basis tracking on a wallet-by-wallet and account-by-account basis under Revenue Procedure 2024-28.

If you are still calculating FIFO across all your wallets as one pool, your cost basis assignments are wrong. When you sell Bitcoin from Kraken, only the lots held in your Kraken account should be in scope. Using a lot that sits in your Coinbase account or Ledger wallet produces an incorrect gain or loss.

This matters because the wrong cost basis can create either an understatement (if you used a higher-basis lot from another wallet, understating your gain) or an overstatement (if you used a lower-basis lot, overstating your gain). An understatement that exceeds the greater of $5,000 or 10% of the tax required to be shown on your return triggers the accuracy-related penalty under IRC §6662: 20% of the underpayment on top of the tax owed, plus interest.

Make sure your cost basis calculations respect the wallet-by-wallet rule. Each exchange account and each wallet has its own lot queue. When you sell, your accounting method draws only from the queue in the account where the sale occurs. If you used a universal method before 2025, Revenue Procedure 2024-28 provided a one-time safe harbor to reallocate basis across your wallets as of January 1, 2025. For a full comparison of how each method works under the wallet-by-wallet rule, see our FIFO, LIFO, and Specific Identification guide.

Mistake #7: Not Answering the Digital Asset Question

Form 1040 includes a yes-or-no question about digital asset activity. For 2025, the question asks whether you received, sold, exchanged, gifted, or otherwise disposed of a digital asset during the year. Every taxpayer must answer it. Leaving it blank is not an option.

Answering "No" when you had reportable crypto activity is a red flag. The IRS can see from your 1099-DA data that you had disposals. A "No" answer that contradicts 1099-DA records is evidence of either negligence or intentional underreporting. The IRS has cited similar discrepancies on the foreign bank account question (Schedule B) as evidence of willfulness in penalty cases.

Note: simply buying crypto with USD does not require a "Yes" answer. Receiving, selling, swapping, spending, gifting, or otherwise disposing of crypto does.

Answer the question honestly. If you had any crypto disposals, staking rewards, airdrops, or other taxable activity in 2025, check "Yes."

Mistake #8: Reporting Proceeds That Don't Match Your 1099-DA

Your 1099-DA shows the gross proceeds from each disposal. The IRS receives the same form. If the proceeds you report on Form 8949, column (d), do not match what your exchange reported, the AUR system flags it.

This mismatch can happen innocently. Maybe you used a different exchange rate. Maybe you manually calculated proceeds from your own records instead of using the 1099-DA figure. Maybe you reported net proceeds (after fees) instead of gross proceeds. Any difference between your Form 8949 and the 1099-DA the IRS has on file creates a potential flag.

Always use the exact proceeds amount from your 1099-DA in column (d) of Form 8949. If you believe the 1099-DA amount is wrong, do not change column (d). Instead, use columns (f) and (g) to make an adjustment with the appropriate code. This way, the IRS sees that you received the 1099-DA and accounted for it, even if you are correcting the basis or reporting a different gain.

What Happens When the IRS Sends a CP2000

If the AUR system flags your return, you will receive a CP2000 notice in the mail. Here is what happens:

The most common resolution for crypto CP2000 notices is that the taxpayer provides cost basis documentation and the proposed assessment is reduced. Many crypto CP2000 notices overstate what is owed because the IRS's automated system assumed zero basis when the 1099-DA did not include it.

The Penalties

Getting a CP2000 notice does not automatically mean you will pay penalties. But certain mistakes do trigger them.

How Cryptofolio Helps

Most of these mistakes come down to one problem: incomplete or inaccurate data. If you do not have accurate cost basis, you cannot fill out Form 8949 correctly. If you cannot match your transfers, you will either report them as sales or lose your cost basis trail. If you do not track DeFi activity, those taxable events go unreported.

Cryptofolio maintains accurate cost basis across all your connected exchanges and wallets in real time. Transfers are automatically matched so cost basis follows the asset. DeFi transactions are parsed and classified. Each wallet has its own lot queue, compliant with the 2025 wallet-by-wallet requirement. When you need to file, the data is already organized by the correct Form 8949 checkbox groups.

The result: fewer mismatches, fewer omissions, and fewer reasons for the IRS to send you a letter.

Don't wait for a CP2000 to find out your records are wrong.

Cryptofolio tracks your cost basis across every wallet and exchange, so your Form 8949 numbers match what the IRS expects.

The Bottom Line

The IRS now has more visibility into crypto transactions than at any point in history. Form 1099-DA gives them the proceeds side of every exchange-based disposal. Their automated systems compare that data against your return. When the numbers do not match, a CP2000 notice follows.

Every mistake on this list is preventable. Report all transactions that appear on your 1099-DA. Supply your own cost basis. Use the correct Form 8949 checkboxes. Track your DeFi activity even though it is not on a 1099-DA. Use wallet-by-wallet cost basis calculations. Answer the digital asset question. Match your reported proceeds to the 1099-DA figures. Many holders don't realize crypto losses can offset gains from other capital assets. See the full rule on crypto losses against stock gains.

The common thread: maintain accurate, complete records before you file. If the IRS sends a notice, the taxpayers who have documentation resolve it quickly. The ones who do not are the ones who end up paying the proposed amount plus penalties.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. While we strive to keep our content accurate and up to date, information in this article may become outdated as policies evolve. Consult a qualified tax professional for advice on your individual circumstances.