How Crypto Airdrops Are Taxed (And Why Most People Get It Wrong)

Crypto airdrops are taxed twice: once as income when you receive them, and again as capital gains when you sell. Here's how the IRS treats them, what most people miss, and how to track them correctly.

You wake up and find 400 $DROP tokens in your wallet that were not there yesterday. You did not buy them. You did not earn them. They just appeared. An airdrop.

Your first instinct is to check the price. Maybe they are worth something. Maybe they are worth nothing. Either way, you now have a tax problem that most people handle incorrectly.

Airdrops are one of the most misunderstood taxable events in crypto. They are taxed twice, at two different rates, at two different times. The first tax hits when you receive the tokens. The second hits when you sell them. Most people either miss the first one entirely or get the second one wrong because they never recorded the right cost basis.

Here is how the IRS actually treats airdrops, and what you need to track to get it right.

Airdrops Are Ordinary Income When Received

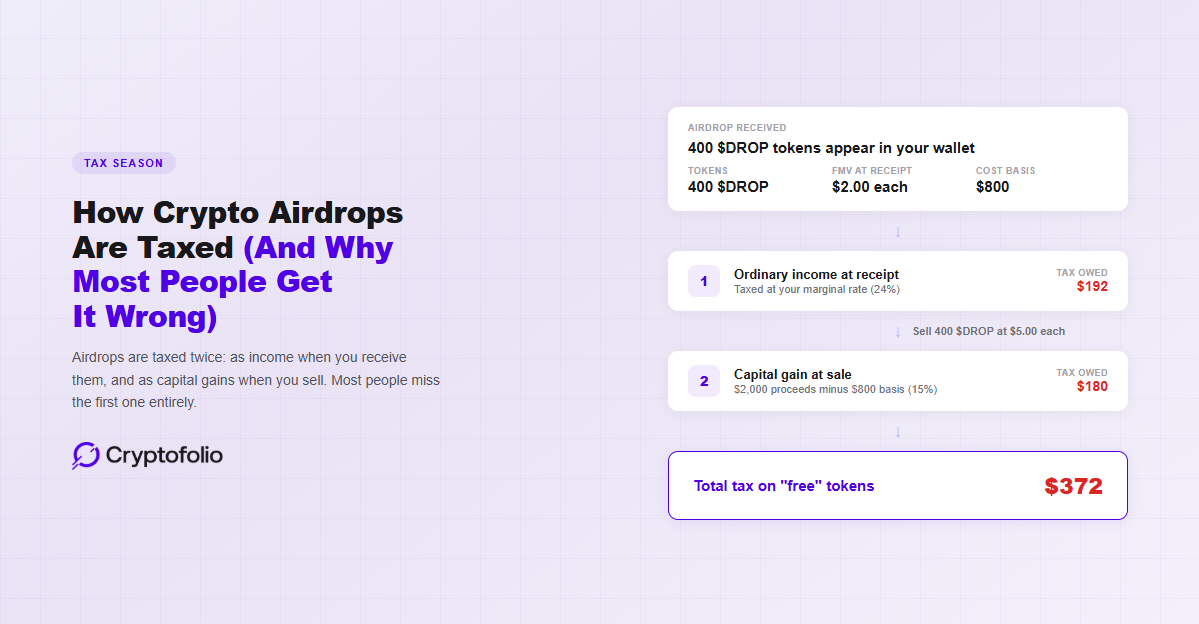

Under Rev. Rul. 2019-24, the IRS treats cryptocurrency received through an airdrop as ordinary income. The taxable amount is the fair market value of the tokens at the time you gain dominion and control over them.

Dominion and control means you can transfer, sell, exchange, or otherwise dispose of the tokens. For most airdrops, that is the moment the tokens appear in your wallet and are recorded on the distributed ledger. If the tokens require you to claim them through a smart contract interaction before they are usable, the income event occurs when you claim them, not when they become available to claim.

This is ordinary income, not a capital gain. It is taxed at your marginal income tax rate, which for most people is significantly higher than the long-term capital gains rate. If you are in the 24% tax bracket, you pay 24% on the value of the airdrop at the time of receipt. If you are in the 32% bracket, you pay 32%. The same ordinary-income-at-receipt mechanic applies to stablecoin yield payments, with slightly different downstream consequences. See stablecoin tax treatment in full.

The amount does not change based on what happens to the token price afterward. If you receive 400 $DROP tokens worth $2 each ($800 total), you have $800 in ordinary income regardless of whether $DROP goes to $10 or drops to zero the next day.

(For more on how the IRS treats different types of crypto income, see our DeFi tax guide.)

The Cost Basis You Need to Record

When you receive airdropped tokens, the fair market value at the time of receipt becomes your cost basis for those tokens.

“If you receive cryptocurrency from an airdrop following a hard fork, your basis in that cryptocurrency is equal to the amount you included in income on your Federal income tax return.” (IRS FAQ)

Using the example above: 400 $DROP tokens received at $2 each means your cost basis is $800 (400 tokens at $2 per token). This is the number you need when you eventually sell, trade, or use those tokens.

If you do not record this cost basis at the time of receipt, you have a problem. When you sell the tokens months or years later, you need to prove what they were worth when you received them to calculate your capital gain or loss correctly. If you cannot prove the cost basis, the IRS can treat it as zero, which means your entire sale proceeds are treated as taxable gain.

This is where most people make their first mistake. They receive the airdrop, do nothing, and move on. No record of the date. No record of the fair market value. No tax lot created. When they eventually sell, they have no basis to report.

What Happens When You Sell

When you sell, trade, or use the airdropped tokens, you have a second taxable event: a capital gain or loss. The calculation is straightforward. Proceeds minus cost basis equals gain or loss.

If you received 400 $DROP tokens at $2 each (cost basis: $800) and later sell all 400 at $5 each ($2,000), your capital gain is $1,200. This is a separate taxable event from the income you recognized when you received them.

If $DROP drops in value after you receive it, you have a capital loss when you sell. If you received tokens worth $800 and sell for $300, you have an $800 income event and a $500 capital loss. The loss can offset other capital gains, and up to $3,000 of excess losses can offset ordinary income per year. (For more on using losses strategically, see our tax-loss harvesting guide.)

Airdrops You Never Claimed

Not every airdrop lands in your wallet automatically. Many require you to visit a website, connect your wallet, and execute a claim transaction. Until you do that, the tokens are available but not in your possession.

The IRS position is that you have income when you gain dominion and control. For unclaimed airdrops, there is a reasonable argument that you do not have dominion and control until you actually claim them. If 400 tokens are allocated to your address but sitting in a claim contract, and you never execute the claim, you have not received them in a tax-relevant sense.

However, this gets complicated if the tokens are directly deposited to your wallet address without any action on your part. In that case, dominion and control likely begins at the moment of deposit, even if you were not aware the airdrop happened. The tokens are in your wallet and you can dispose of them.

The practical implication: if you claim an airdrop, the income event occurs at the time of the claim transaction, not when the airdrop was first announced or made available. Record the fair market value at the time of the claim. If tokens arrive directly in your wallet without a claim step, the income event occurs at the time of deposit.

Airdrops Worth Nothing (or Nearly Nothing)

Some airdrops have no liquid market at the time of receipt. The token might not be listed on any exchange. There might be no reliable price data. In that case, the fair market value at receipt could reasonably be assessed at $0 or near $0.

If the FMV at receipt is $0, you have $0 in ordinary income and a cost basis of $0. When you eventually sell (if the token gains value), the entire proceeds are capital gains.

This is actually a better tax outcome than receiving tokens with significant value at receipt. You skip the ordinary income tax entirely and only pay capital gains tax when you sell. The question is whether you can defensibly claim the FMV was zero. If the token was trading on any exchange or had any observable market price at the time you received it, claiming zero is not defensible. You need to record whatever the market price was, even if it was a fraction of a cent.

Keep documentation of the price (or lack thereof) at the time of receipt. A screenshot of the token on a DEX showing no liquidity, a CoinGecko page showing no price data, or the absence of any trading pair is all useful evidence if you need to support a zero or near-zero valuation.

Hard Forks vs. Promotional Airdrops

The IRS uses the term “airdrop” in Rev. Rul. 2019-24 specifically in the context of hard forks, where a blockchain splits and holders of the original token receive tokens on the new chain. But the same tax principles apply to promotional airdrops, governance token distributions, retroactive rewards, and any other situation where you receive tokens without paying for them.

The mechanics are the same in every case: ordinary income at fair market value when received, cost basis set at that same FMV, and capital gain or loss when you eventually dispose of the tokens.

The one exception is if you receive tokens as compensation for a specific service, such as a bounty program where you write content or test software in exchange for tokens. In that case, the tokens are still ordinary income at FMV when received, but they may also be subject to self-employment tax if the arrangement constitutes freelance work. Standard airdrops distributed to all holders of a token or all users of a protocol are not considered compensation for services and are not subject to self-employment tax.

The Tracking Problem

Airdrops create a unique tracking challenge. Unlike a purchase, where you know exactly when you bought and what you paid, an airdrop arrives without a clear transaction on your side. You did not initiate it. You may not know exactly when it appeared. You may not check the price until days or weeks later.

For each airdrop, you need to record four things at the time of receipt: the date and time the tokens were received or claimed, the number of tokens received, the fair market value per token at that exact time, and the total ordinary income amount (quantity times FMV).

This creates a new tax lot in your portfolio with a cost basis equal to the income recognized. Every subsequent transaction involving those tokens (selling, trading, using, or even transferring to another wallet) needs to reference this lot for accurate gain or loss calculation.

If you received multiple airdrops of the same token at different times, each one is a separate lot with its own cost basis and holding period. When you sell, your accounting method (FIFO, LIFO, or Specific Identification) determines which lot is consumed first, which affects whether the gain is short-term or long-term. (For more on accounting methods, see our FIFO vs. LIFO guide.)

The complexity multiplies when airdrops arrive across multiple wallets or chains. If you received the same token airdrop on Ethereum and Arbitrum because you had activity on both chains, each wallet has its own lot queue under the IRS per-wallet tracking requirement (Rev. Proc. 2024-28). Selling the tokens from your Ethereum wallet consumes different lots than selling from your Arbitrum wallet.

(For more on per-wallet tracking requirements, see our transfer guide.)

Common Airdrop Tax Mistakes

Not reporting the income at receipt. This is the most common mistake. People treat airdropped tokens as free money with no tax obligation until they sell. The IRS says otherwise. The income is taxable the moment you gain dominion and control, regardless of whether you sell.

Using the wrong price for cost basis. Some people use the price on the day they first noticed the airdrop, not the day they received it. If tokens arrived on March 5 but you did not check until March 12, the fair market value on March 5 is what matters. Using the March 12 price gives you the wrong income amount and the wrong cost basis.

Not creating a tax lot for the airdrop. If your portfolio tracker does not recognize the airdrop as an income event and create a lot with the correct cost basis, every subsequent sale of those tokens will have incorrect gain or loss. The error compounds if you received the airdrop months or years before selling.

Ignoring the gas fee on the claim transaction. If you had to execute a claim transaction, the gas fee is a separate taxable disposal of the token used to pay gas (usually ETH). That gas fee runs through your FIFO lot queue for the native token. It is a small amount per transaction, but it is a real cost that affects your P&L. (For more on how gas fees are taxed, see our cost basis guide.)

Treating all airdrops as capital gains. The income at receipt is ordinary income, not a capital gain. These are taxed at different rates. Lumping everything into “gains” misclassifies the income and produces the wrong tax category on your return.

How Cryptofolio Handles Airdrops

Cryptofolio classifies airdrops as income events automatically. When tokens appear in your wallet via an airdrop, the system records the fair market value at the time of receipt, recognizes the income, and creates a new tax lot with the correct cost basis.

For claim-based airdrops, the income is recognized at the time of the claim transaction, not when the tokens became available. The gas fee on the claim transaction is tracked as a separate disposal through your native token's FIFO lot queue.

Each airdrop lot is tracked per wallet and per chain. If you received the same token on multiple chains, each wallet maintains its own lot queue in compliance with Rev. Proc. 2024-28. When you sell, the correct lots are consumed based on your accounting method and the wallet you are selling from.

For tokens with no observable market price at the time of receipt, Cryptofolio flags the transaction for your review so you can assign a fair market value (including $0 if that is the defensible position) rather than silently ignoring the income event.

Airdrops are not free. They are income the moment you receive them.

Cryptofolio tracks every airdrop as an income event, records the fair market value at receipt, creates the correct tax lot, and maintains accurate cost basis for when you eventually sell.

The Bottom Line

Airdrops are taxed twice. Once as ordinary income when you receive them at the fair market value on that date. Once as a capital gain or loss when you eventually sell, calculated against the cost basis set at receipt.

Most people miss the first event entirely. They receive tokens, do nothing, and only think about taxes when they sell. By that point, the fair market value at receipt is hard to determine, the cost basis was never recorded, and the P&L on the sale is wrong.

The fix is recording four data points at the time of every airdrop: the date, the quantity, the fair market value per token, and the total income amount. Those four numbers create the tax lot that makes everything else work correctly.

If your tracker does not classify airdrops as income events and create lots with the correct cost basis, you are building your portfolio on incomplete data. And every transaction involving those tokens going forward will inherit that gap.

(For more on how different types of crypto income are tracked, see our DeFi tax guide and our DeFi cost basis guide. For a broader look at why P&L calculations go wrong, see our P&L tracker guide.)

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, financial, or investment advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. While we strive to keep our content accurate and up to date, information in this article may become outdated as policies evolve. Consult a qualified professional for advice on your individual circumstances.