The SEC Just Classified Every Major Crypto Asset. Here's What It Means for Investors.

The SEC and CFTC jointly declared that most crypto assets are not securities. Here's the new five-category token taxonomy, which assets are classified, and what it means for your portfolio.

On March 17, 2026, the SEC and CFTC jointly issued the most significant regulatory clarification in the history of digital assets. After more than a decade of ambiguity, enforcement actions, and the "regulation by enforcement" approach under the previous administration, the two agencies published a 68-page interpretation that formally classifies crypto assets and draws clear lines between what falls under securities law and what doesn't.

The headline: most crypto assets are not securities.

"After more than a decade of uncertainty, this interpretation will provide market participants with a clear understanding of how the Commission treats crypto assets under federal securities laws. It also acknowledges what the former administration refused to recognize: that most crypto assets are not themselves securities."

This is published as a final rule in the Federal Register, not informal guidance. It is a joint interpretation with the full weight of both agencies. The CFTC confirmed it will administer the Commodity Exchange Act consistent with the SEC's classification. Both agencies signed off.

Here's what you need to know.

The Five Categories

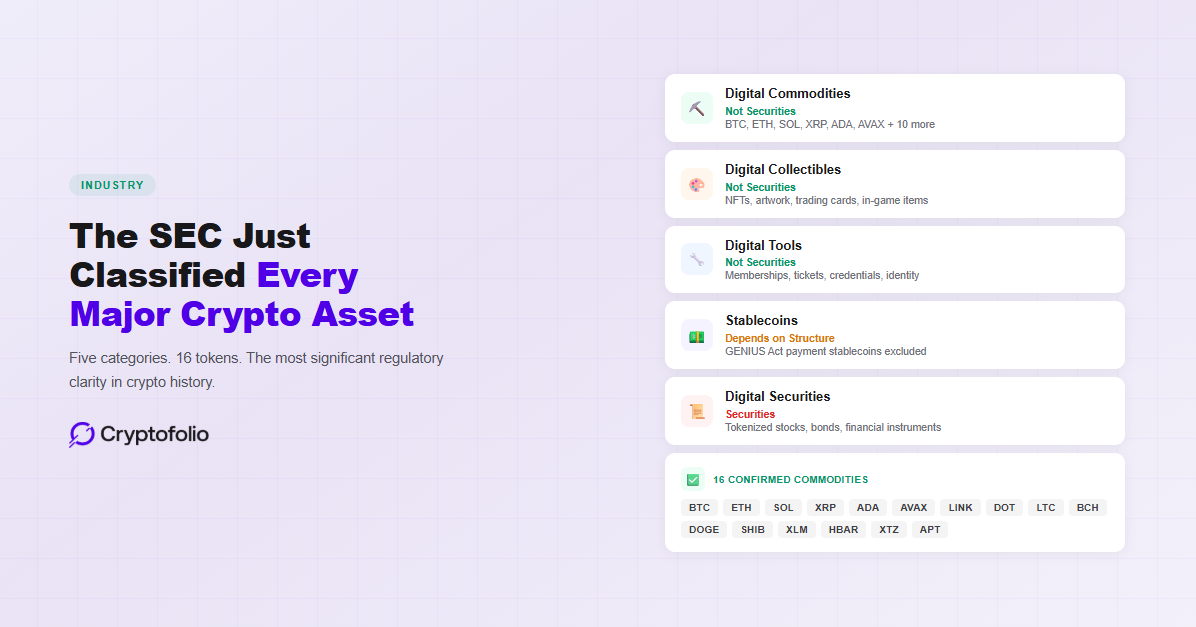

The interpretation establishes a formal token taxonomy. Every crypto asset falls into one of five categories based on its characteristics, use, and function.

Digital Commodities. These are crypto assets that derive their value from the operation of a functional crypto network and from supply and demand, not from the expectation of profits based on someone else's managerial efforts. They are not securities. The SEC explicitly named 16 assets in this category: Bitcoin (BTC), Ether (ETH), Solana (SOL), XRP, Cardano (ADA), Avalanche (AVAX), Chainlink (LINK), Polkadot (DOT), Litecoin (LTC), Bitcoin Cash (BCH), Dogecoin (DOGE), Shiba Inu (SHIB), Stellar (XLM), Hedera (HBAR), Tezos (XTZ), and Aptos (APT).

Digital Collectibles. NFTs and similar assets that represent or convey rights to artwork, music, videos, trading cards, in-game items, or digital representations of memes, characters, or trends. Not securities.

Digital Tools. Crypto assets that perform a practical function, such as a membership, ticket, credential, title instrument, or identity badge. Not securities.

Stablecoins. Payment stablecoins issued by a permitted issuer under the GENIUS Act are not securities. Other stablecoins may or may not be, depending on their structure.

Digital Securities. Traditional financial instruments (stocks, bonds, etc.) that happen to be represented as crypto assets. These are securities and remain under SEC jurisdiction.

The first three categories are definitively not securities. Stablecoins depend on their structure. Only digital securities remain under the SEC's purview.

Why This Matters

For years, the core question in crypto regulation was whether any given asset was a security. The answer determined which agency had jurisdiction, which rules applied, and whether an exchange could list the asset without registering as a securities exchange.

Under the previous SEC chair, the agency took the position that virtually all crypto assets could be securities and pursued over 125 enforcement actions totaling more than $6 billion in penalties. Solana, XRP, and Cardano were all subject to SEC scrutiny. That era is now formally over.

The practical implications for investors:

Regulatory clarity means more products. Spot Bitcoin ETFs have attracted tens of billions in inflows since launching in January 2024. Spot Solana and XRP ETFs followed in late 2025, both seeing strong institutional demand. With 16 assets now formally classified as commodities, the path for additional ETF products targeting assets like Cardano, Chainlink, and Polkadot is significantly clearer.

Exchange operations simplify. US exchanges can now list these 16 assets with certainty about their regulatory status. The CFTC has clear jurisdiction over spot markets for digital commodities. This removes the legal overhang that previously forced exchanges to delist assets or operate in uncertainty.

Institutional participation grows. The single biggest barrier to institutional crypto adoption has been regulatory ambiguity. Fund managers, corporate treasuries, and insurance companies need to know whether holding an asset triggers securities registration, reporting, and compliance obligations. For the 16 named digital commodities, that question is answered.

What It Says About Staking, Mining, Airdrops, and Wrapping

Beyond the taxonomy, the interpretation directly addresses four activities that had been in a regulatory gray area for years.

Protocol staking (validating transactions by locking tokens on a proof-of-stake network) is classified as an administrative or ministerial activity. It does not constitute the offer and sale of a security. This applies to native staking where you are directly participating in network consensus.

Protocol mining (the computational work validators perform on proof-of-work networks) receives the same treatment. Mining activities are not securities transactions.

Airdrops (free distributions of tokens to wallet holders) generally do not involve an "investment of money" under the Howey test. If you didn't pay money or provide services in exchange for the tokens, the airdrop itself is not a securities transaction.

Wrapping a non-security crypto asset (converting ETH to WETH, for example) does not transform the underlying asset into a security. The wrapped version retains the same classification as the original.

These clarifications remove uncertainty around activities that millions of crypto users engage in regularly.

What This Does NOT Change

This is the part most likely to be misunderstood.

The SEC's interpretation is about securities classification. It determines which agency has jurisdiction and which rules apply at the federal regulatory level. It does not change how you are taxed.

The IRS still treats all crypto as property. Whether the SEC calls Bitcoin a digital commodity, a digital collectible, or something else entirely, the IRS treats every digital asset as property under existing tax law. That means every sale, swap, and disposal is a taxable event. Every staking reward is ordinary income at fair market value when you receive it. Every airdrop is income when you gain dominion and control. This was true before March 17, and it is true after.

Staking rewards are still taxable income. The SEC saying that staking is not a securities transaction does not mean staking rewards are tax-free. Under Revenue Ruling 2023-14, staking rewards are taxable as ordinary income at fair market value when the taxpayer gains dominion and control. Nothing in the SEC's interpretation changes this. (For the full breakdown of how staking, swaps, LPs, and airdrops are taxed, see our DeFi tax guide.)

Airdrops are still taxable income. The SEC saying that an airdrop is not a securities transaction has no bearing on the IRS treatment. Under IRS guidance, airdropped tokens are ordinary income at fair market value when you can access them. The fair market value at receipt becomes your cost basis for future sales.

The wash sale exemption still holds. The SEC formally classifying crypto as non-securities actually reinforces the current tax treatment. The wash sale rule under IRC §1091 applies only to "stock or securities." With the SEC now confirming that most crypto assets are digital commodities and not securities, the argument that crypto is exempt from wash sale rules is stronger than before. You can still sell crypto at a loss, claim the deduction, and immediately repurchase the same asset. (For details on how to use this strategy, see our tax-loss harvesting guide.)

Cost basis rules are unchanged. The wallet-by-wallet tracking requirement under Revenue Procedure 2024-28, the FIFO default, Specific Identification under Notice 2025-7, and every other IRS cost basis rule remains exactly the same. The SEC's classification doesn't affect how you track, calculate, or report your gains and losses. (For a full comparison of accounting methods, see our FIFO vs. LIFO guide.)

Form 1099-DA reporting is unchanged. Centralized exchanges still report gross proceeds to the IRS on Form 1099-DA for 2025 disposals. The SEC's classification doesn't affect broker reporting obligations under the IRS's digital asset regulations.

Investment Contracts Can Now End

One of the most structurally important parts of the interpretation is the clarification that investment contracts can terminate.

Under the previous framework, if a token was ever offered as part of an investment contract (a fundraising event where buyers expected profits from the issuer's efforts), it was treated as being subject to securities laws indefinitely. There was no clear path out.

The new interpretation provides two ways an investment contract can end:

Fulfillment. The issuer completes the essential managerial efforts it represented or promised to undertake. Once those promises are fulfilled, the token is no longer subject to the investment contract.

Failure. The issuer publicly and unequivocally abandons its intention to complete the promised efforts. The investment contract terminates because there are no longer any managerial efforts from which investors would expect profits.

In both cases, the underlying non-security crypto asset returns to its natural classification (digital commodity, digital collectible, or digital tool). This creates a defined pathway for projects to "graduate" from securities law compliance, which didn't exist before.

What Comes Next

The interpretation is a bridge. In his speech at the DC Blockchain Summit, Chairman Atkins stated that the Commission expects to release a proposed rule for public comment "in the coming weeks." That proposal would include a startup exemption, a fundraising exemption, and an investment contract safe harbor. Atkins is calling this "Regulation Crypto Assets," and the framework draws directly from Commissioner Hester Peirce's Token Safe Harbor proposal first introduced in 2020.

Meanwhile, Congress has already passed the GENIUS Act, which President Trump signed into law on July 18, 2025, establishing the first federal regulatory framework for payment stablecoins. The interpretation's stablecoin category aligns directly with the GENIUS Act's definitions. The next legislative priority is the CLARITY Act, which would give the CFTC exclusive jurisdiction over digital commodity spot markets. The CLARITY Act passed the House in July 2025, but the Senate Banking Committee has not yet completed its markup. The interpretation is designed to serve as the regulatory framework until that legislation is enacted.

What This Means for Portfolio Tracking

For anyone managing a crypto portfolio across wallets, exchanges, and DeFi protocols, this interpretation changes the regulatory backdrop but not the practical requirements.

You still need accurate cost basis across every asset you hold. You still need to track lot-level data per wallet under the IRS's wallet-by-wallet rule. You still need to account for staking rewards, airdrops, gas fees, and DeFi interactions as taxable events.

What does change is the regulatory environment around the infrastructure being built to serve you. With clearer rules, more institutional products, and a defined taxonomy, the tools and services available to crypto investors will improve. Exchanges will offer better reporting. ETF products will expand. And portfolio trackers that maintain accurate cost basis across all five asset categories will become more important, not less, as the market matures.

The rules are getting clearer. Your tracking should be too.

Cryptofolio tracks your cost basis across every wallet, exchange, and chain, whether your holdings are digital commodities, DeFi positions, NFTs, or stablecoins.

The Bottom Line

March 17, 2026, is the day the SEC formally acknowledged what the crypto industry has argued for years: most crypto assets are not securities. The five-category token taxonomy, the joint CFTC coordination, the staking and airdrop clarifications, and the investment contract termination framework represent the most comprehensive regulatory clarity the US crypto market has ever received.

For investors, this is a structural positive. Clearer rules mean broader access, more products, and less legal risk for platforms and service providers.

But it does not change your tax obligations. The IRS treats crypto as property regardless of how the SEC classifies it. Your cost basis still matters. Your accounting method still matters. Your records still matter.

The regulatory environment just got significantly better. Make sure your portfolio tracking keeps up.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, financial, or investment advice. Regulatory frameworks are evolving rapidly, and the interpretation discussed in this article may be subject to future revisions, rulemaking, or legislative changes. Consult a qualified professional for advice on your individual circumstances.