What Happens to Your Cost Basis When You Wrap Crypto

Wrapping ETH to WETH or BTC to WBTC may or may not be a taxable event. The IRS hasn't ruled on it. Here's how both positions work, what happens to your cost basis either way, and why your tracker probably gets it wrong.

You wrap ETH to WETH to use it on a DEX. You wrap BTC to WBTC to use it on Ethereum. The token changes. Your economic exposure does not. You still hold the same value, the same amount, backed by the same underlying asset.

The question is whether the IRS sees it the same way. As of April 2026, the IRS has not told us. There is no statute, no case law, and no published IRS guidance that definitively states whether wrapping a token is a taxable event.

That leaves two positions. Both are defensible. Both have real consequences for your cost basis and your P&L. Your tracker needs to handle both correctly, or your numbers are wrong from the moment you wrap.

What Wrapping Actually Does

When you wrap a token, you deposit the original asset into a smart contract. The contract locks your deposit and mints a new token that represents it on a 1:1 basis. ETH goes in, WETH comes out. BTC goes in, WBTC comes out.

The wrapped version exists so the original asset can interact with protocols and standards it was not designed for. ETH does not conform to the ERC-20 standard that most Ethereum DeFi protocols require. WETH does. BTC does not exist on Ethereum at all. WBTC does.

Unwrapping reverses the process. You send the wrapped token back to the contract, it burns the wrapped version, and returns the original asset. WETH goes in, ETH comes out.

From an economic standpoint, nothing changed. You held 1 ETH before. You held 1 WETH during. You held 1 ETH after. Your exposure to the price of ETH never changed. No new asset was created in the way a swap produces something fundamentally different.

From a technical standpoint, you interacted with a smart contract that minted a new token with a different contract address. That is a different asset on the blockchain, even if it represents the same underlying value.

This distinction is where the tax treatment gets complicated.

The Two Positions

The conservative position treats wrapping as a crypto-to-crypto swap. Under this view, depositing ETH and receiving WETH is a disposal of ETH and an acquisition of WETH. You recognize a capital gain or loss based on the difference between your cost basis in the ETH and its fair market value at the time of the wrap. The WETH receives a new cost basis equal to its FMV at receipt.

If you bought ETH at $1,800 and wrap it when ETH is at $3,000, you recognize a $1,200 capital gain at the time of wrapping. Your WETH now has a cost basis of $3,000. When you later unwrap and sell the ETH, you calculate gains against that $3,000 basis.

This approach is more likely to hold up under IRS scrutiny if the agency eventually rules that wrapping is taxable, because you have already recognized the gain. It also simplifies record-keeping if you wrap and unwrap frequently, since each step resets the basis.

The downside: you may be paying tax on a transaction that the IRS may later rule was not taxable. And if you wrap and unwrap within the same day at effectively the same price, you are generating taxable events with minimal actual economic change.

The alternative position treats wrapping as a non-taxable transfer. Under this view, wrapping is analogous to moving crypto between your own wallets. Your economic position has not changed. You are the same owner holding economically equivalent exposure to the same underlying asset. No gain or loss is recognized. Your original cost basis carries through to the wrapped token.

If you bought ETH at $1,800 and wrap it when ETH is at $3,000, your WETH inherits the $1,800 cost basis. When you later unwrap and sell at $3,500, your gain is calculated against $1,800, not $3,000.

Many tax practitioners favor this position for simple same-chain wrapping (ETH to WETH on Ethereum) because the substance of the transaction has not changed. The form changed, but the economics did not. This argument is stronger when the peg is 1:1 and the wrapped token is redeemable at any time for the original asset.

The risk: if the IRS eventually rules that wrapping is taxable, you would owe tax on gains that should have been recognized at the time of wrapping. You might also owe interest and penalties on the underpayment.

What the IRS Has Actually Said

Not much.

Notice 2024-57 exempts wrapping and unwrapping transactions from broker reporting requirements. Brokers are not required to file Forms 1099-DA for these transactions until the IRS issues further guidance. For a full breakdown of how the 1099-DA rules affect DeFi reporting, see our complete DeFi tax guide.

The reporting exemption "does not constitute or reflect a substantive analysis for Federal income tax purposes of any of the identified transactions." The IRS delayed reporting because it has not figured out the tax treatment, not because it decided wrapping is non-taxable.

There is no Revenue Ruling, Revenue Procedure, or published IRS guidance that addresses wrapping specifically. The closest precedent is general property tax principles under Notice 2014-21 (crypto is property, dispositions trigger gain or loss) and the broader question of whether exchanging one digital asset for another that tracks the same value constitutes a taxable exchange.

Tax attorneys have called for standardized guidance on wrapping. Until it arrives, both positions remain defensible as long as you apply your chosen approach consistently across all wrapping transactions and document your reasoning.

Where Cost Basis Breaks

Regardless of which tax position you take, the cost basis needs to be tracked correctly. Here is where most trackers fail.

If you take the conservative position (taxable swap), the tracker needs to recognize the wrap as a disposal of ETH with gain/loss, create a new lot for WETH at FMV, and later recognize the unwrap as another disposal of WETH with its own gain/loss. That is two taxable events for what feels like one round trip. Most trackers either do not recognize wrapping as a taxable event or they misclassify it.

If you take the alternative position (non-taxable transfer), the tracker needs to carry the original cost basis from ETH to WETH without creating a taxable event, then carry it back from WETH to ETH when you unwrap. The wrapped and unwrapped versions must be treated as economically equivalent. Most trackers do not understand that WETH and ETH are the same underlying asset, so they treat the wrap as a sale of ETH and a purchase of WETH with a new basis at FMV.

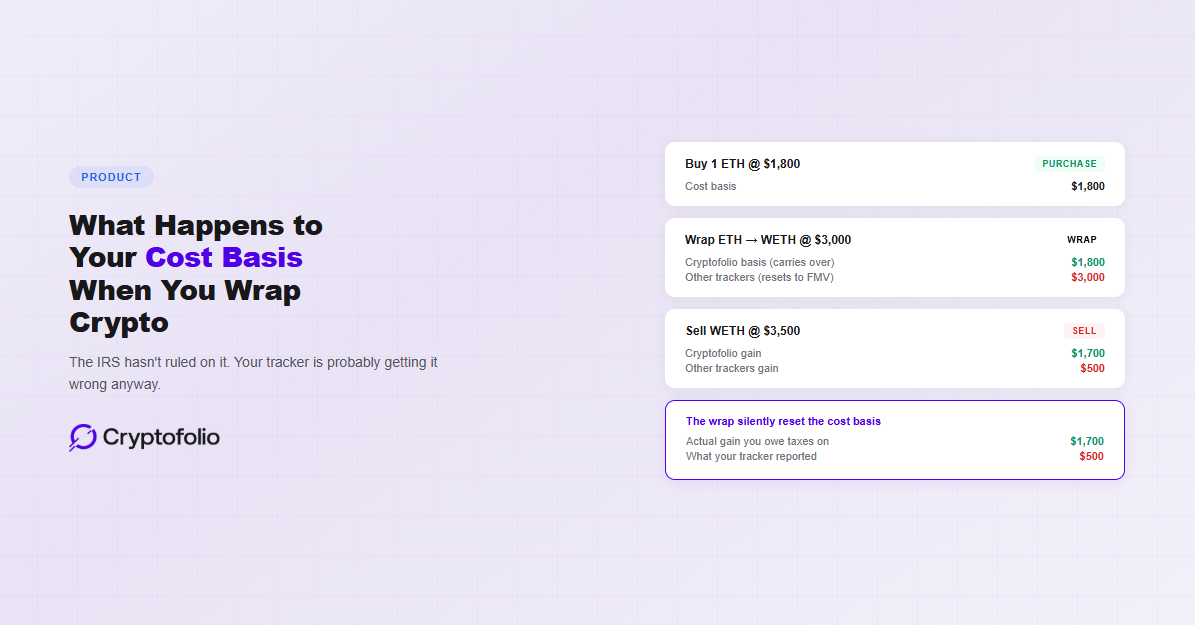

The second scenario is the more common problem. A tracker that treats every wrap as a new purchase at market price silently resets your cost basis. If you originally bought ETH at $1,200 and wrap it when ETH is $3,000, the tracker gives WETH a basis of $3,000. When you unwrap and sell at $3,500, the tracker shows a $500 gain instead of the $2,300 gain you actually owe. Your P&L is wrong, your tax reporting is wrong, and you do not know it because the numbers still look reasonable on screen. For a broader look at the most common sources of calculation errors, see our guide on why your crypto P&L is wrong.

The DeFi Chain Reaction

Wrapping rarely happens in isolation. You wrap ETH to WETH to make a swap on Uniswap. You wrap BTC to WBTC to deposit into an Aave lending pool. The wrap is the first step in a multi-step DeFi interaction, and if the cost basis breaks at the wrap, everything downstream is wrong. For a detailed walkthrough of how each DeFi interaction transforms your cost basis from that point forward, see our DeFi cost basis guide.

Consider a typical DeFi sequence: you wrap 1 ETH (bought at $1,800) to WETH when ETH is $3,000. You swap 0.5 WETH for USDC on Uniswap. You deposit 0.5 WETH into Aave as collateral.

Under the transfer position (non-taxable wrap), your WETH carries the $1,800 basis. The Uniswap swap is the first taxable event: you dispose of 0.5 WETH with a $900 basis and receive USDC at $1,500 FMV, realizing a $600 gain. The Aave deposit may or may not be taxable depending on your position on lending deposits.

Under the conservative position (taxable wrap), you already recognized a $1,200 gain at the wrap. Your WETH has a $3,000 basis. The Uniswap swap now shows a $0 gain (disposing of $1,500 FMV WETH with a $1,500 basis). The total tax outcome is the same over time, but the timing of when you recognize the gain differs.

A tracker that silently resets the basis at the wrap under the transfer position reports the $600 gain on the swap as $0 (because it thinks the basis is $1,500) and the error propagates downstream. Gas fees paid for each of these interactions are also separate disposals running through your FIFO lot queue. For a detailed breakdown of how gas fees consume lots on every DeFi interaction, see our gas fees cost basis guide.

Cross-Chain Wrapping

Same-chain wrapping (ETH to WETH on Ethereum) is the simplest case. Cross-chain wrapping adds complexity because the wrapped token exists on a different blockchain entirely.

Wrapping BTC to WBTC involves locking BTC with a custodian and receiving WBTC on Ethereum. BitGo serves as the custodian for WBTC, holding BTC in reserve on a 1:1 basis. The original BTC is held in custody. The WBTC token is a separate contract on a separate chain.

The non-taxable transfer argument is weaker here because you are not just changing the form of the token. You are introducing counterparty risk (the custodian), changing the blockchain, and receiving a token with different liquidity characteristics and potentially different pricing.

For cross-chain wrapping through bridges (like wrapping ETH to receive WETH on Avalanche), the analysis overlaps with cross-chain bridge treatment. We covered that in detail in our guide to how bridging affects your cost basis.

The conservative position is more commonly recommended for cross-chain wrapping. The alternative position becomes harder to defend when the destination token has materially different characteristics from the original. For a broader look at how errors in your cost basis compound through your portfolio, see our guide on how to calculate and fix your cost basis.

How Cryptofolio Handles Wrapping

Cryptofolio recognizes the relationship between wrapped and unwrapped tokens. When you wrap ETH to WETH, the tracker understands these are economically equivalent assets and carries the original cost basis forward without creating a taxable event. This matches the non-taxable transfer position that most practitioners recommend for simple same-chain wrapping.

If you need to report under the conservative position (treating wrapping as a taxable swap), Cryptofolio records the FMV at the time of wrapping so you have both numbers available. You can file under either interpretation with accurate data for both.

The wrapped token inherits the original acquisition date and lot position in your FIFO queue. When you later use the WETH in a DeFi interaction, the gain or loss calculation uses the correct original basis, not a silently reset market price.

For cross-chain wrapping, Cryptofolio connects the outgoing transaction on one chain with the incoming wrapped token on another, the same way it handles cross-chain bridges. The cost basis follows across chains regardless of whether the token symbol changed.

Most trackers silently reset your cost basis when you wrap. Cryptofolio does not.

Cryptofolio recognizes the relationship between wrapped and unwrapped tokens, carries your original cost basis through every wrap and unwrap, and records FMV data so you can file under either tax position with accurate numbers.

The Bottom Line

Wrapping is one of the most common DeFi interactions and one of the least understood from a tax perspective. The IRS has not ruled on it. Both the conservative (taxable swap) and alternative (non-taxable transfer) positions are defensible. What matters is that you pick one approach, apply it consistently, and make sure your tracker handles it correctly.

Most trackers do not. They either treat every wrap as a new purchase at market price (silently resetting your basis) or ignore the transaction entirely (leaving a hole in your transaction history). Either way, every DeFi interaction after the wrap inherits the error.

Your cost basis should survive a wrap. If your tracker cannot maintain it, everything downstream is built on the wrong number.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, financial, or investment advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. The tax treatment of wrapping and unwrapping transactions remains unsettled, and different tax professionals may take different positions. Consult a qualified tax professional for advice on your individual circumstances.