What Happens to Your Cost Basis When You Bridge Crypto

Bridging crypto between chains creates one of the messiest cost basis problems in portfolio tracking. Here's what actually happens to your numbers and why most trackers get it wrong.

You buy ETH on Ethereum. You bridge it to Avalanche. Same asset, same amount, same you. But on the other side, your cost basis is gone.

That is the reality for most crypto portfolio trackers. The bridge creates a gap that the tracker cannot cross, and everything downstream of that gap is wrong. Your P&L, your unrealized gains, your tax numbers. All of it built on a missing foundation.

Bridging is one of the most common actions in DeFi, and it creates one of the most persistent cost basis problems in crypto. Not because the tax treatment is complicated (though it is genuinely unsettled), but because the infrastructure most trackers rely on cannot follow your assets across chains.

What Actually Happens When You Bridge

A bridge moves your crypto from one blockchain to another. The mechanics vary by bridge protocol, but the basic pattern is the same: you deposit an asset on the source chain, and receive a corresponding asset on the destination chain.

Sometimes the bridge locks your original tokens and mints a wrapped version on the other side. Sometimes it burns tokens on one chain and mints native tokens on the other. Sometimes it uses liquidity pools on both ends.

From your portfolio's perspective, the outcome is the same. You had 1 ETH on Ethereum. Now you have 1 ETH (or WETH, or ETH.e) on Avalanche. Your holdings have not changed. Your exposure has not changed. But the on-chain record now shows two separate events on two separate blockchains, with no native connection between them.

This is where cost basis breaks.

Why Most Trackers Lose the Thread

When you bridge ETH from Ethereum to Avalanche, here is what a typical portfolio tracker sees:

On Ethereum: a token left your wallet. It looks like a send, a swap, or a contract interaction depending on how the bridge protocol structures the transaction.

On Avalanche: a token appeared in your wallet. It looks like a receive from an unknown source.

The tracker has no way to connect those two events. It does not know the token that arrived on Avalanche is the same token that left Ethereum. So it does one of three things.

It assigns the incoming token a cost basis of $0, which inflates your gains when you eventually sell. It uses the market price at the time of arrival as the cost basis, which creates a phantom purchase that never happened. Or it flags the transaction as unresolved and leaves you to figure it out.

None of those are correct. Your cost basis is whatever you originally paid for that ETH, plus any fees. The bridge did not change that. It just moved the asset to a different chain.

Your cost basis should follow your crypto across chains. If it does not, every calculation after the bridge is built on the wrong number.

Is Bridging a Taxable Event?

The IRS has not issued specific guidance on cross-chain bridges. That leaves two reasonable interpretations, and the right answer depends on the mechanics of the bridge and how you characterize the transaction.

The conservative position treats a bridge as a taxable exchange. You disposed of ETH on Ethereum and acquired a different asset (wrapped ETH, ETH.e, or a bridge-specific token) on Avalanche. Under this view, you would recognize a gain or loss at the time of the bridge based on the difference between your cost basis and the fair market value of the asset at that moment. The new token's cost basis would reset to its FMV at the time you received it.

The alternative position treats a bridge as a non-taxable transfer, similar to moving crypto between your own wallets. You are the same owner, holding economically equivalent exposure to the same underlying asset. Under this view, no gain or loss is recognized, and the original cost basis carries over to the destination chain.

Tax practitioners are split on which position is correct. Some recommend the conservative approach on the basis that it is more defensible if the IRS eventually rules that bridges are taxable exchanges. Others argue that for simple bridges where you are moving the same asset between chains for your own use, the transfer analogy holds. The logic mirrors how the IRS treats transfers between brokerage accounts in traditional finance: moving an asset does not change your basis in it.

One relevant reference point: IRS Notice 2024-57 temporarily exempts wrapping and unwrapping transactions from broker reporting requirements under Form 1099-DA. That exemption covers the mechanics of wrapping a token (exchanging ETH for WETH, for example), but does not directly address cross-chain bridge transactions that use different mechanisms like lock-and-mint or liquidity pools. The Notice explicitly states that the reporting exemption does not reflect any substantive analysis of how these transactions should be treated for tax purposes.

The safe approach: track both the original cost basis (carrying it over as if it were a transfer) and the fair market value at the time of the bridge (in case you need to treat it as a disposal). A good tracker should give you both numbers so you can file under either interpretation.

The Bridge Fee Problem

Regardless of which tax position you take on the bridge itself, the fees are a separate issue.

Bridge fees typically come in two forms. There is a gas fee on the source chain to initiate the transaction, and sometimes a protocol fee charged by the bridge itself.

Gas fees paid in a native token (like ETH) are a disposal of that token. The IRS treats gas fees as taxable dispositions (IRS FAQ A53). If you pay 0.005 ETH in gas to bridge your tokens, that 0.005 ETH is consumed from your FIFO lot queue. If the oldest ETH lot in your wallet was purchased at $1,200 and ETH is now worth $3,000, that 0.005 ETH disposal generates a small capital gain.

Most people ignore this. Over dozens of bridge transactions, the cumulative impact adds up. For active DeFi users bridging between multiple chains regularly, uncounted gas disposals can represent hundreds of dollars in untracked gains or losses. For a full explanation of how gas fees affect your cost basis across every transaction type, including bridges, see our gas fees guide.

Protocol fees work differently depending on the bridge. Some deduct from the amount bridged (you send 1 ETH, you receive 0.997 ETH). Some charge a flat fee in a separate token. Either way, the fee needs to be accounted for in your cost basis calculation on the destination side.

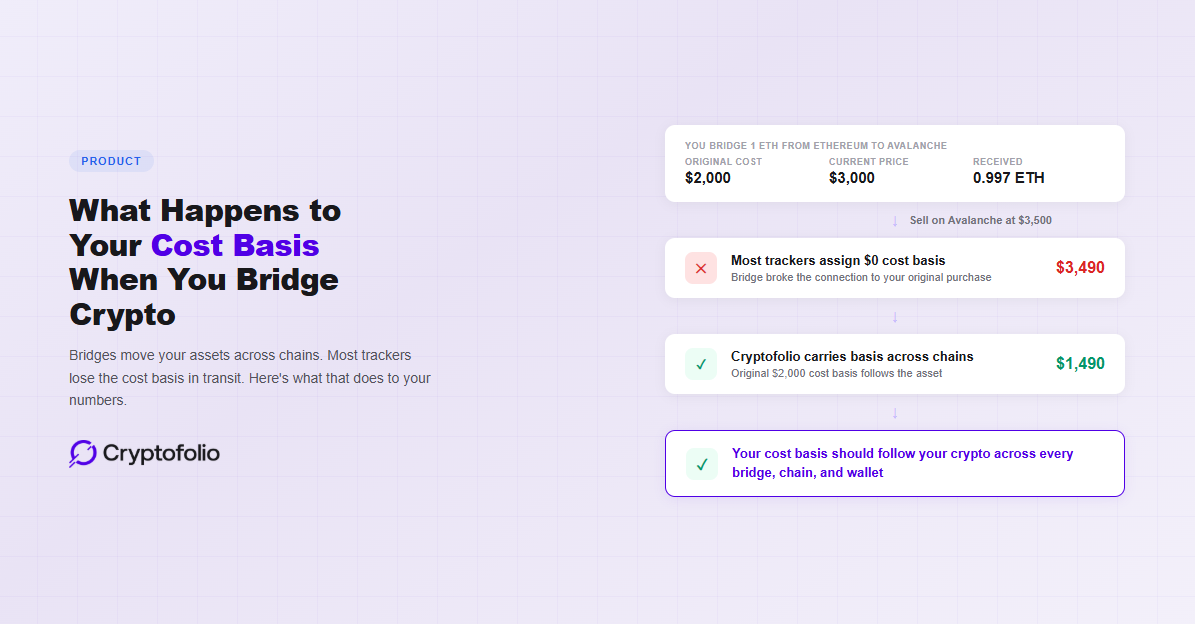

A Real Example: What the Numbers Look Like

You buy 2 ETH on Coinbase at $2,000 each. Total cost basis: $4,000. You transfer both to your MetaMask wallet on Ethereum. Cost basis carries over: still $4,000.

You bridge 1 ETH to Avalanche using a bridge protocol. The bridge charges a 0.3% protocol fee, and you pay 0.004 ETH in gas on Ethereum. ETH is currently trading at $3,000.

Here is what should happen to your cost basis:

The gas fee (0.004 ETH) is a disposal. Under FIFO, it comes from your oldest lot. At a $2,000 cost basis and a current market price of $3,000, that is a realized gain of $4.00 on the gas disposal. Your remaining ETH on Ethereum drops from 2.000 to 0.996 ETH.

On Avalanche, you receive 0.997 ETH (1.000 minus the 0.3% bridge fee). If you are treating the bridge as a non-taxable transfer, the cost basis for that 0.997 ETH is carried over from the original purchase. You paid $2,000 for the 1 ETH that was bridged. That $2,000 basis now applies to the 0.997 ETH on the destination chain. The 0.003 ETH bridge fee reduces your quantity but does not create a separate taxable event under the transfer interpretation.

Your portfolio now looks like this:

Now imagine you sell all 0.997 ETH on Avalanche at $3,500 per ETH. That is $3,490.50 in proceeds.

With the correct cost basis ($2,000), your capital gain is $1,490.50.

On a single transaction. Multiply that across a portfolio with dozens of bridge events, and the error compounds into thousands of dollars.

What Happens When You Bridge Back

The return trip creates the same problem in reverse. You bridge your 0.997 ETH from Avalanche back to Ethereum. Another gas fee, another protocol fee, another pair of disconnected on-chain events.

If your tracker lost the cost basis on the way over, it has nothing to work with on the way back. The ETH arrives on Ethereum with no history attached. When you eventually sell on a centralized exchange, that exchange has no idea what you paid for it.

This is the same pattern that breaks cost basis in wallet-to-wallet transfers, but bridges make it worse. Transfers at least stay on the same chain, where a tracker can potentially match the send and receive by transaction hash or timing. Bridges cross chains entirely, which means there is no shared ledger to reconcile against.

Maintaining cost basis across a bridge requires the tracker to recognize the bridge transaction on both chains, connect the outgoing and incoming events, carry the cost basis forward, and account for fees on both sides. Most trackers do not attempt this at all.

Wrapped Tokens and Cost Basis

Bridges often produce wrapped versions of the original token. You bridge ETH to Avalanche and receive WETH.e. You bridge USDC to Polygon and receive USDC.e. The token symbol changes, the contract address is different, and from a purely on-chain perspective, it is a completely different asset.

For portfolio tracking purposes, this creates an additional layer of complexity. A tracker needs to understand that WETH.e on Avalanche is economically equivalent to ETH on Ethereum. If it treats them as separate assets, your portfolio shows a sale of ETH and a purchase of WETH.e, each with its own cost basis. That is wrong under the transfer interpretation for the same reason: you did not change your economic position.

The IRS has not issued specific guidance on whether wrapping or unwrapping tokens is a taxable event. Notice 2024-57 exempts these transactions from broker reporting, but explicitly states that the exemption does not reflect any determination of their tax treatment. Tax practitioners are divided. The conservative position treats wrapping as a crypto-to-crypto swap that triggers a gain or loss. The alternative position treats it as a non-taxable event because the economic substance has not changed.

The same issue applies when you unwrap. Converting WETH back to ETH on any chain should, under the transfer interpretation, carry the cost basis through. If the tracker does not recognize the relationship between wrapped and unwrapped tokens, it breaks the chain again. For a full walkthrough of how wrapping affects your cost basis, including both tax positions and where most trackers break, see our wrapping guide. For how these interactions change your cost basis at each step in a DeFi session, see our DeFi cost basis guide.

How Cryptofolio Handles Bridges

Cryptofolio treats bridge transfers as non-taxable movements of the same asset, carrying the original cost basis forward to the destination chain. This matches the transfer interpretation that many practitioners use for simple bridges where the user is moving their own assets between chains.

When you bridge ETH from Ethereum to Avalanche, Cryptofolio connects the outgoing transaction on Ethereum with the incoming transaction on Avalanche. Your original acquisition date and cost basis transfer to the new chain. The bridge fee and gas costs are tracked separately as their own line items in your transaction history, with gas fees running through the FIFO lot queue as disposals.

If the automated matching cannot confidently connect two sides of a bridge (because the bridge protocol is unsupported or the transaction structure is unusual), Cryptofolio surfaces it for review. You can manually link the send and receive transactions, and the cost basis follows. No spreadsheet required.

Cost basis that follows your crypto across chains.

Cryptofolio connects bridge transactions on both sides, carries your original cost basis to the destination chain, and tracks fees so your P&L is right no matter where your assets move.

Why This Matters Beyond Taxes

Even if you are not thinking about taxes right now, broken cost basis from bridges corrupts every other number in your portfolio.

Your P&L is wrong because the tracker thinks you acquired the bridged tokens at the wrong price. Your unrealized gains are wrong because the cost basis is either zero or inflated. Your portfolio performance over time is wrong because the tracker cannot distinguish between actual gains and artifacts of missing data.

If you have ever looked at your portfolio app and seen a return figure that did not match your gut feeling, bridges are one of the most common causes. The tracker lost the thread somewhere in the middle of a cross-chain movement, and every number after that point inherited the error. For a broader look at how missing data like this distorts the numbers in your portfolio app, see our guide on what your portfolio app is not telling you.

For anyone managing assets across multiple chains and wallets, tracking this correctly is what separates a reliable portfolio picture from one built on gaps. For a guide on tracking crypto across multiple wallets and chains without losing your cost basis, see our multi-wallet tracking guide.

The Bottom Line

Bridges do not change what you own. They do not change what you paid. They just move your assets to a different chain. But for most portfolio trackers, that movement is enough to break the one number that matters most: your cost basis.

The fix is not complicated in theory. Connect the send and the receive. Carry the basis forward. Account for the fees. But doing it across chains, across bridge protocols, and across wrapped token variants requires infrastructure that most trackers have not built.

If you are active in DeFi and you are bridging between chains, check whether your tracker actually follows your cost basis across those bridges. If it does not, your P&L has been wrong since the first time you bridged.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. The tax treatment of cross-chain bridge transactions and wrapped token exchanges remains unsettled, and different tax professionals may take different positions. Consult a qualified tax professional for advice on your individual circumstances.