How to Track DeFi Positions Across Multiple Protocols

Your DeFi positions are scattered across Aave, Uniswap, Lido, and a dozen other protocols. Here's why most trackers miss them and what to look for in one that doesn't.

You have ETH staked on Lido. A lending position on Aave. Liquidity in a Uniswap v3 pool. Some SOL earning yield through Jito. A few tokens sitting in a Curve gauge you forgot about six months ago.

You know you have DeFi positions. What you probably do not know is how much they have actually made you. Or cost you.

That is the gap between seeing your DeFi balances and actually tracking your DeFi portfolio. Most tools do the first part well. Almost none do the second part at all.

The Problem with DeFi Tracking

DeFi positions are fundamentally different from tokens sitting in a wallet or on an exchange. A token has a quantity and a price. Multiply them together and you have a value. Simple.

A DeFi position is not simple. When you deposit ETH into Aave, you receive aETH. The aETH balance increases over time as interest accrues. When you withdraw, you get back more ETH than you deposited. Between deposit and withdrawal, the original ETH does not exist as a token in your wallet anymore. It has been replaced by a receipt token that represents a claim on the underlying asset plus earned interest.

When you provide liquidity on Uniswap v3, you deposit two tokens into a specific price range and receive an NFT representing your position. The composition of your position changes continuously as trades move through your price range. When you withdraw, you may get back a completely different ratio of the two tokens than what you put in. And if the price moved outside your range entirely, one side of your position may have been fully converted into the other token.

When you stake ETH through Lido and receive stETH, your stETH balance rebases daily. Each rebase increment may be taxable income at the fair market value when received. If you then use that stETH as collateral on Aave, you now have a staked position inside a lending position, and both are generating yield simultaneously.

Each of these interactions creates multiple data points that a tracker needs to capture: the deposit, the receipt token, the yield accrual, the withdrawal, and the tax classification of each step. Most tools capture some of these. Very few capture all of them correctly.

What Most DeFi Trackers Actually Show You

The most popular DeFi tracking tools, including DeBank, Zerion, and Zapper, are designed to answer one question: what do I currently hold across my DeFi positions?

They do this well. DeBank supports over 800 protocols across 15+ blockchains. Zerion integrates with 500+ protocols. Both can detect your LP positions, staking positions, lending positions, and claimable rewards across multiple chains in real time. Connect your wallet, and you see a dashboard of everything you have deployed.

What they do not show you is what any of those positions have actually earned or cost you.

DeBank does not track cost basis. It does not calculate realized or unrealized gains on your DeFi positions. It does not maintain lot-level records. It does not classify yield as income at the fair market value when received. As a 2026 review put it, DeBank is “a research and monitoring layer rather than a complete finance stack.”

Zerion offers P&L tracking through its Premium subscription and calculates gains using FIFO at the wallet level. For token positions, this gives you a useful picture of whether you are up or down. But Zerion is primarily a monitoring and action layer, not a full accounting system. It does not classify staking rewards as taxable income at the fair market value when received. It does not maintain per-wallet lot queues that comply with the IRS wallet-by-wallet requirement. It does not produce the kind of transaction-level cost basis records you need for Form 8949. A 2026 review described it as useful for tracking “what is held, where it is held, and what positions are active,” but noted that “users who need tax-lot accounting” should look elsewhere.

CoinStats tracks DeFi positions across 90+ wallets and 10 networks, but its DeFi tracking focuses on balance aggregation rather than transaction-level accounting. It shows what you hold in each protocol. It does not reconstruct the full lifecycle of each position for accurate P&L.

These are all useful tools. But they are balance viewers for DeFi, not portfolio trackers for DeFi.

For a comparison of how established tax tools like Koinly and CoinTracker handle DeFi versus a portfolio tracker built for continuous tracking, see our Koinly vs CoinTracker vs Cryptofolio guide.

Why Balance Viewing Is Not Enough

Knowing what you currently hold in a DeFi protocol is one piece of the picture. Knowing what you made or lost requires significantly more data.

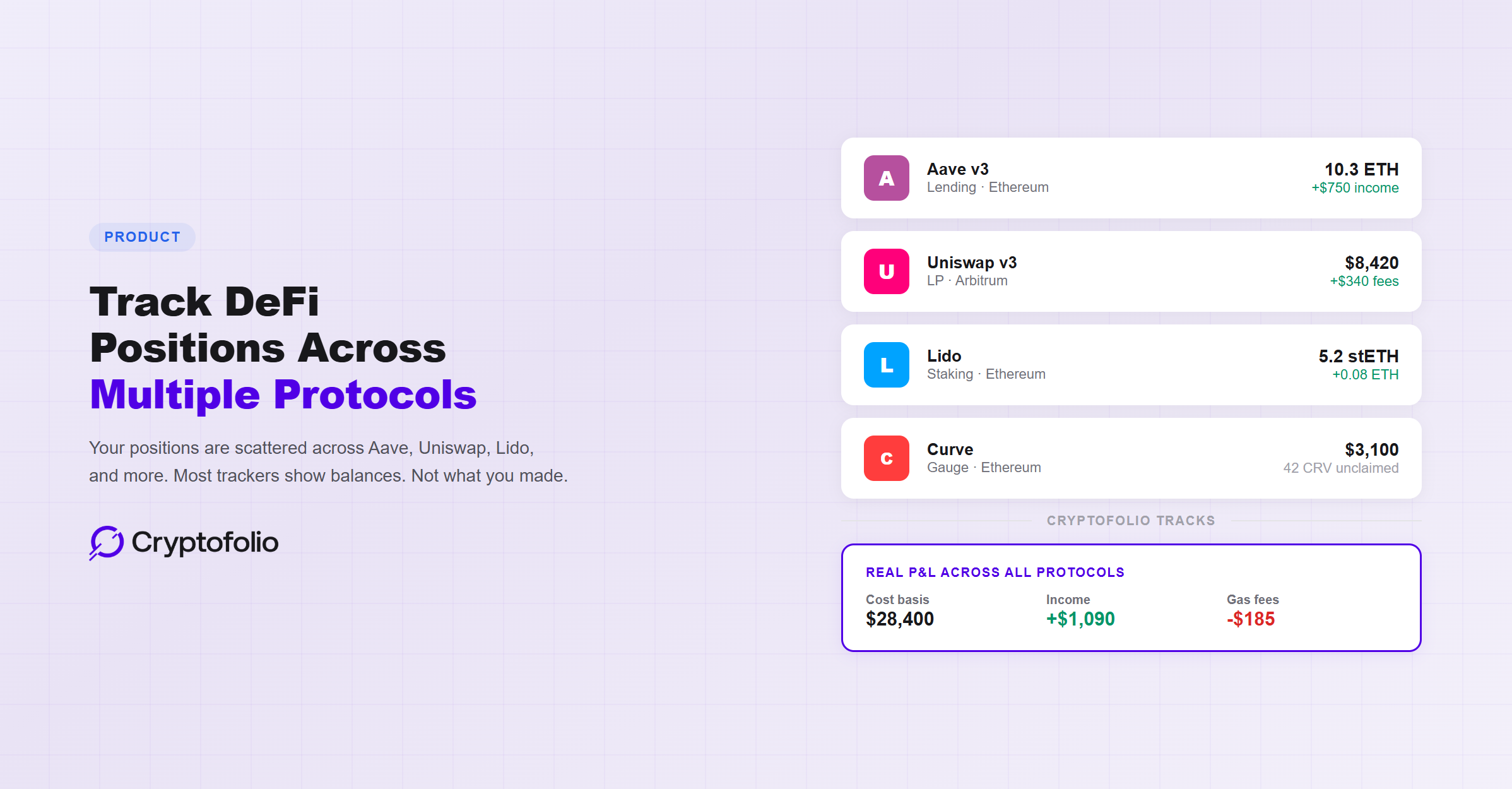

Consider a straightforward Aave lending position. You deposit 10 ETH when ETH is at $2,000. Over six months, you earn 0.3 ETH in interest while the price rises to $3,000. You withdraw all 10.3 ETH.

The balance tracker gives you one number. The portfolio tracker gives you the full financial picture, and every number in it matters when you file your taxes or evaluate whether the position was actually worth the risk.

For a full breakdown of how DeFi interactions are taxed, see our DeFi tax guide. For a broader look at the five most common reasons DeFi activity causes P&L to go wrong, see our P&L tracker guide.

The Specific Challenges of Multi-Protocol Tracking

If tracking one DeFi position is complex, tracking positions across multiple protocols on multiple chains is an order of magnitude harder. Here is where it breaks down.

Each protocol has its own mechanics. Aave uses rebasing receipt tokens (aTokens). Uniswap v3 uses NFTs to represent concentrated liquidity positions. Lido uses rebasing liquid staking tokens (stETH). Curve uses gauge deposits with CRV reward emissions. Each protocol represents positions, accrues yield, and handles withdrawals differently. A tracker that understands Aave's mechanics cannot assume the same logic applies to Uniswap or Curve. Each protocol needs its own classification logic. For a deep dive into how tracking lending positions on Aave and Compound works — including the differences between V3 aTokens, V2 cTokens, Compound III, and the new Aave V4 share model — see our lending position tracking guide.

Positions span multiple chains. You might have Aave positions on Ethereum, Base, and Avalanche simultaneously. The same protocol, deployed on different chains, with different gas costs, different token addresses, and different transaction formats. A tracker needs to parse each chain's data independently while maintaining a unified view of your total Aave exposure.

Yield accrues in different ways. Some protocols increase your token balance over time (Aave's aTokens, Lido's stETH). Others distribute separate reward tokens (Curve's CRV emissions, Convex's CVX). Others accumulate yield inside the position itself without changing your balance (Uniswap v3 fees). Each accrual method has different tax treatment and needs different tracking logic.

Composed positions create nested complexity. Using stETH as collateral on Aave means you have a staking position inside a lending position. The stETH is earning staking yield while simultaneously serving as collateral. Both need to be tracked. If you borrow against that collateral and deploy the borrowed tokens into another protocol, you now have three layers of positions to reconcile.

Gas fees accumulate across every interaction. Every deposit, withdrawal, claim, and approval transaction costs gas. For active DeFi users making dozens of transactions per week across multiple chains, cumulative gas fees can run into thousands of dollars. Each gas payment is a taxable disposal of the native token (ETH, AVAX, SOL) that runs through your FIFO lot queue. A tracker that ignores gas costs is ignoring a real and potentially significant line item in your P&L.

For more on how gas fees affect your cost basis, see our cost basis guide.

What to Look for in a DeFi Portfolio Tracker

Not every tool that shows DeFi positions is actually tracking them. Here is what separates balance viewing from real portfolio tracking.

Protocol-level transaction parsing. The tracker needs to understand what each protocol interaction means, not just that tokens moved. An Aave deposit is not a transfer to another person. An LP withdrawal is not a sale. A staking reward is not a purchase. If the tracker cannot distinguish between these transaction types, it will misclassify them, and your P&L will be wrong.

Cost basis that carries through DeFi interactions. When you deposit ETH into Aave, the cost basis of that ETH needs to follow it into the position. When you withdraw, the cost basis needs to come back out and attach to the returned tokens. If cost basis resets to fair market value every time you interact with a protocol, your gain and loss calculations will be inaccurate. For a step-by-step walkthrough of how cost basis changes at each DeFi interaction, from Aave deposits and withdrawals to Uniswap swaps and Lido staking, see our DeFi cost basis guide. For more on how cost basis works across transfers and protocol interactions, see our transfer guide.

Income recognition at the right moment. Staking rewards, lending interest, and liquidity pool fees are all income events. The IRS treats them as ordinary income at fair market value when you gain dominion and control (Rev. Rul. 2023-14 for staking rewards). A tracker needs to identify when yield is received, record the fair market value at that moment, and create a new tax lot with that value as the cost basis for future sales. For a deep dive into how staking rewards create new lots, why the frequency of rewards matters, and how liquid staking tokens complicate tracking, see our guide on tracking staking rewards across wallets.

Per-wallet lot tracking. Under Revenue Procedure 2024-28, cost basis must be tracked on a wallet-by-wallet basis. Your Aave position on Ethereum and your Aave position on Avalanche are in different wallets with separate FIFO lot queues. A tracker that pools DeFi positions across chains into one global calculation is not compliant with current IRS requirements. For a full explanation of the wallet-by-wallet rule, see our FIFO vs. LIFO guide.

Handling for unsupported protocols. No tracker covers every protocol on every chain. What matters is how the tool handles a protocol it does not yet support. Does it silently ignore the transaction? Does it misclassify it as a generic transfer? Or does it flag it for your review so you can manually classify it and enter the correct cost basis? The difference between those three approaches is the difference between wrong data, misleading data, and honest data.

Fee tracking as a first-class feature. Gas fees on DeFi transactions are not a footnote. They are taxable events that affect your P&L. A tracker that treats fees as invisible is hiding real costs from your performance numbers.

For a broader look at all six criteria that separate a real portfolio tracker from a balance viewer, see our portfolio tracker buyer's guide.

Common DeFi Tracking Mistakes

Even with a capable tool, DeFi tracking goes wrong in predictable ways.

Treating LP deposits as sales. Adding tokens to a liquidity pool is generally treated as disposing of those tokens and acquiring LP tokens. Some trackers treat the deposit as a sale to an external address, generating a phantom taxable gain. The correct treatment is to record it as a disposal with acquisition of the LP token at the same fair market value. LP positions also carry additional complexity that most trackers miss entirely — underlying composition shifts, separate fee accrual on V3, and impermanent loss against a simple hold baseline. For a deep dive into what trackers get wrong about liquidity pool positions, see our LP tracking guide.

Missing claimable rewards. Rewards that have accrued but not been claimed are not yet taxable. Income recognition happens when you gain dominion and control, which for most protocols means when you claim. A tracker that records unclaimed rewards as income is overstating your tax liability. A tracker that never records them even after you claim is understating it.

Ignoring wrapped and receipt tokens. When you deposit ETH and receive aETH, the aETH is a new asset with its own cost basis: the fair market value of the ETH you deposited. When you later sell or transfer aETH, you need to calculate gain or loss against that basis. Trackers that do not recognize receipt tokens as distinct assets will produce incorrect P&L.

Double-counting across chains. If you bridge stETH from Ethereum to Arbitrum, a tracker that does not recognize the bridge might show you holding stETH on both chains temporarily, doubling your apparent balance. Worse, it might treat the bridge as a sale on Ethereum and a new purchase on Arbitrum, generating a phantom gain and resetting your cost basis. For more on how bridges affect your cost basis, see our transfer guide.

How Cryptofolio Handles DeFi Tracking

Cryptofolio treats DeFi as a first-class part of your portfolio, not an afterthought bolted onto a balance viewer.

Every supported protocol gets its own parsing logic. An Aave deposit is classified as a lending position entry, not a transfer. A Uniswap LP deposit is classified as a liquidity provision event, not a sale. Staking rewards are recorded as income at fair market value when claimed. Each protocol interaction is parsed according to what it actually is, not approximated as a generic token movement.

Cost basis follows your assets through every DeFi interaction. When you deposit ETH into a protocol, the FIFO lot that gets consumed carries its original acquisition date and purchase price into the position record. When you withdraw, that basis comes back. Your P&L reflects what you actually paid, not what the token happened to be worth on the day you interacted with the protocol.

For protocols that Cryptofolio does not yet support, transactions are flagged in the UI for your review rather than silently ignored or incorrectly classified. You can manually classify the transaction type and enter cost basis. When the protocol is later added to Cryptofolio's supported list, typically within 12 to 24 hours of the request, the on-chain data replaces your manual entry automatically.

Gas fees on every DeFi interaction are tracked as first-class ledger data. Each gas payment runs through your wallet's FIFO lot queue for the native token, and the resulting gain or loss is included in your P&L.

All of this is tracked per wallet, per chain, in compliance with the IRS wallet-by-wallet requirement under Revenue Procedure 2024-28.

DeFi positions are part of your portfolio. Track them like it.

Cryptofolio parses DeFi protocol interactions and maintains accurate cost basis across staking, lending, liquidity pools, and more.

The Bottom Line

DeFi gives you access to yield, liquidity, and financial tools that did not exist five years ago. It also gives you a tracking problem that most portfolio tools are not designed to solve.

Knowing what you hold across Aave, Uniswap, Lido, and Curve is the easy part. Knowing what each position cost you, what it earned you, what fees you paid along the way, and what you owe in taxes requires a fundamentally different kind of tracking. It requires understanding each protocol's mechanics, maintaining cost basis through every interaction, recognizing income at the right moment, and tracking everything per wallet.

If your current tool shows you DeFi balances but cannot answer the question “how much did this position actually make me,” it is showing you the surface. The numbers that matter are underneath.

Protocol risk adds another dimension that most DeFi trackers are not built for. For more on what happens when a protocol gets hacked and what it means for your tracked balance, P&L, and tax records, see our DeFi exploit guide. For a broader look at what separates a balance tracker from a portfolio tracker, see our portfolio tracker explainer and our comparison guide.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, financial, or investment advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. While we strive to keep our content accurate and up to date, information in this article may become outdated as policies evolve. Consult a qualified professional for advice on your individual circumstances.