How to Track Crypto Staking Rewards Across Wallets

Every staking reward creates a new tax lot with its own cost basis and holding period. Here's why tracking them across wallets is harder than it looks, and what most trackers miss.

Every time you receive a staking reward, a new tax lot is created. It has its own cost basis (the fair market value at the moment you received it), its own holding period, and its own future gain or loss when you eventually sell. If you are staking across multiple wallets and protocols, you are generating dozens or hundreds of these lots per year. Most portfolio trackers do not track them at all.

That is the problem. Staking rewards are not just income. They are inventory. Each one becomes a separate entry in your FIFO lot queue, with a unique cost basis tied to a specific price at a specific moment. When you sell staked tokens months later, the gain or loss on each lot depends on what the price was when that specific reward hit your wallet. Get the receipt price wrong, miss a reward entirely, or lump them all together, and your P&L is off.

(For a full explanation of how FIFO lot queues work and how the accounting method you choose affects your tax bill, see our FIFO vs. LIFO guide.)

What Happens When You Receive a Staking Reward

The IRS treats staking rewards as ordinary income at fair market value the moment you gain dominion and control over them (Rev. Rul. 2023-14). “Dominion and control” means the moment you can sell, exchange, or otherwise dispose of the tokens. Not when you withdraw them. Not when you sell them. When they become available to you.

This means every staking reward triggers two things simultaneously. First, it is income. The fair market value at receipt is taxable as ordinary income in the year you receive it. Second, it creates a new tax lot. That FMV becomes the cost basis for the tokens. When you sell them later, your capital gain or loss is calculated against that basis.

If you earned 0.05 ETH in staking rewards when ETH was trading at $2,400, you have $120 in ordinary income. That 0.05 ETH now sits in your lot queue with a cost basis of $120. If ETH rises to $3,500 and you sell, your capital gain is calculated against the $120 basis, not whatever ETH costs today.

This is straightforward for a single reward on a single protocol. It gets complicated fast when you are staking across multiple wallets.

Jarrett v. United States (3:24-cv-01209, M.D. Tenn.) is an active case challenging whether staking rewards should be taxable at receipt. Cross-motions for summary judgment were due April 10, 2026, with a bench trial scheduled for September 29, 2026 if not resolved on summary judgment. Until there is a ruling, Rev. Rul. 2023-14 remains the current IRS position and the standard that taxpayers should follow.

Why Multiple Wallets Make This Harder

Most people who stake do not do it in one place. You might have ETH staked through Lido on Ethereum, SOL staked through a native validator on Solana, positions on Aave generating lending interest, and tokens staked through Jupiter or Jito. Each of these produces rewards on its own schedule, in its own token, at its own price point.

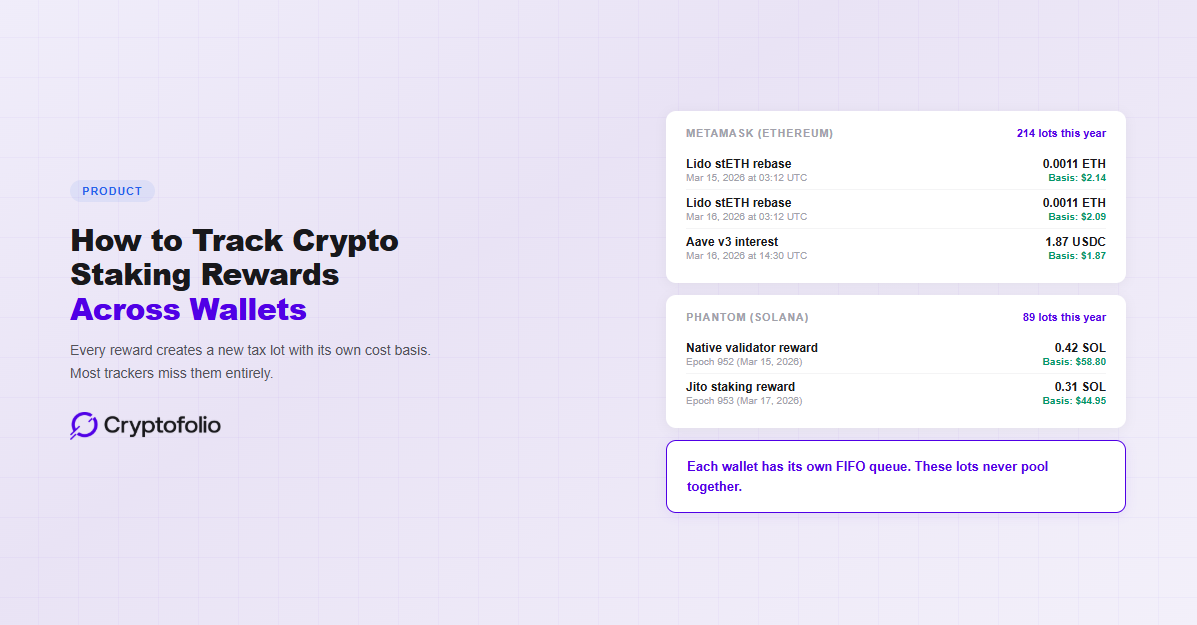

Under IRS rules (Rev. Proc. 2024-28), cost basis must be tracked on a per-wallet basis. That means staking rewards received in your MetaMask wallet create lots that belong to MetaMask's lot queue. Rewards received in your Phantom wallet belong to Phantom's queue. They do not pool together. When you sell from a specific wallet, FIFO consumes the oldest lot in that wallet, not the oldest lot across your entire portfolio.

A tracker that aggregates all your staking rewards into one global view might show the right total income. But the lot queue is wrong. The per-wallet basis is wrong. And when you sell from one wallet, the gain calculation pulls from the wrong queue.

(For more on how cost basis must be maintained across multiple wallets and what breaks when it is not, see our guide to tracking DeFi positions and our DeFi cost basis guide.)

The Frequency Problem

Staking rewards do not arrive once a quarter like a stock dividend. Depending on the protocol, they can arrive every few seconds, every block, every epoch, or at irregular intervals.

Ethereum validators earn consensus layer rewards every epoch, which is roughly every 6.4 minutes. These rewards accumulate in the validator's balance and are swept to the withdrawal address approximately every 8 days. The taxable event under Rev. Rul. 2023-14 occurs when the reward accrues to the validator's balance (the point of dominion and control), not when the sweep delivers it to the withdrawal address.

Solana validators and delegators earn rewards at the end of each epoch, approximately every 2 days. Rewards are distributed in the first block of the following epoch and automatically compound into the staker's balance.

Aave lending interest accrues continuously and is reflected in your aToken balance in real time. Lido stETH rebases daily, incrementing your balance to reflect earned rewards.

Each increment is a separate income event with its own FMV at the time of receipt. Over a year, an active staker can accumulate hundreds or thousands of individual reward lots, each with a slightly different cost basis depending on what the price was at that exact moment.

No human is tracking this manually. And most portfolio trackers are not tracking it at all. They either ignore staking rewards entirely, record them as a single lump sum at an arbitrary price, or only capture them when you withdraw rather than when you receive them.

Liquid Staking Makes It Worse

Liquid staking protocols like Lido (stETH), Rocket Pool (rETH), and Coinbase (cbETH) add another layer of complexity, and they do not all work the same way.

When you deposit ETH into Lido, you receive stETH. The consensus among tax practitioners is that this is a taxable exchange under IRC Section 1001 (disposing of ETH, acquiring stETH at FMV), though the IRS has not issued guidance specific to liquid staking mechanics. As your stETH balance rebases upward each day to reflect earned rewards, each increment is a separate income event under the conservative tax position. That means holding stETH can generate 365 income recognition events per year, each creating a new lot with its own cost basis.

Protocols like Rocket Pool handle this differently. rETH does not rebase. Instead, the exchange rate between rETH and ETH increases over time as rewards accumulate. Because the token balance does not change, there is no periodic income event to recognize. Under this model, the embedded rewards are not taxed until you redeem rETH for ETH, at which point the gain is treated as capital gains rather than ordinary income. This is a significant structural advantage for tax-conscious stakers.

The tracking requirements depend entirely on which type of liquid staking token you hold. A tracker that applies the same logic to both rebasing and exchange-rate tokens will get the tax classification wrong for one of them.

Restaking Compounds the Problem

Restaking protocols like EigenLayer and ether.fi on Ethereum, and Jito on Solana, take staked assets and stake them again across additional services. Each layer can generate its own rewards, in its own token, on its own schedule.

If you deposit ETH into Lido to get stETH, then deposit stETH into EigenLayer, and then deposit the resulting position into ether.fi, you now have three layers of staking activity. Each layer may produce separate reward tokens. Each reward is a separate income event with its own cost basis. And the cost basis of the underlying ETH needs to flow through every layer without breaking.

Most trackers cannot handle even the first layer properly. By the time you are three layers deep, the cost basis trail has usually broken completely.

What Most Trackers Get Wrong

The common failures follow a pattern.

Some trackers do not classify staking rewards as income at all. They treat them like transfers or deposits, which means no income is recognized and no new lot is created. Your tax reporting is incomplete and your future sale calculations use the wrong basis.

Some trackers record staking rewards but use the wrong price. They might use the price at the time of daily sync instead of the price at the moment of receipt. If your tracker syncs once a day but you received rewards at 3am when the price was 4% lower, every lot basis is slightly off. Over hundreds of rewards, that adds up.

Some trackers lump all rewards together into periodic summaries. Instead of creating individual lots for each reward event, they aggregate rewards into daily or weekly totals. This simplifies the display but produces incorrect lot-level basis data. When you sell specific tokens later, the FIFO queue does not match reality.

Some trackers only capture rewards when you claim or withdraw them, not when you receive them. For protocols where rewards auto-compound or accrue in real time (like Aave's aTokens or Lido's stETH rebases), the taxable event happens at receipt, not at withdrawal. A tracker that waits for withdrawal is recording income in the wrong tax year.

(For a broader look at why P&L numbers go wrong across DeFi portfolios, see our guide on why your crypto P&L is wrong. For what to look for when choosing a tracker that handles this correctly, see our portfolio tracker guide.)

What Correct Tracking Looks Like

Accurate staking reward tracking requires four things.

The tracker needs to classify each reward as ordinary income at the moment of receipt. Not at withdrawal. Not at sale. At receipt. The FMV at that moment determines both the income amount and the cost basis of the new lot.

The tracker needs to create a separate lot for each reward event. That lot belongs to the wallet where the reward was received. It enters that wallet's FIFO queue with its own acquisition date and cost basis.

The tracker needs to handle protocol-specific mechanics. Rebasing tokens (stETH), exchange-rate tokens (rETH), aToken balance increments (Aave), and native staking rewards all behave differently on-chain. The tracker needs to interpret each correctly rather than applying a one-size-fits-all classification.

The tracker needs to maintain all of this per wallet. Staking rewards on your MetaMask wallet do not merge with rewards on your Phantom wallet. Each wallet has its own independent lot queue, and sales from each wallet consume lots from that specific queue.

(For a walkthrough of how cost basis flows through each DeFi interaction, from staking deposits to rebase increments to withdrawals, see our cost basis guide and our DeFi tax guide.)

How Cryptofolio Tracks Staking Rewards

Cryptofolio classifies staking rewards as ordinary income at FMV at the time of receipt and creates a new tax lot for each event. The income amount and cost basis are recorded at the moment the reward hits your wallet, not when you claim or withdraw.

Each reward lot is assigned to the wallet where it was received. It enters that wallet's FIFO lot queue with its own acquisition date and holding period. When you sell from that wallet, FIFO consumes the oldest lots first, including any staking reward lots that have aged past the one-year threshold for long-term capital gains treatment.

For liquid staking protocols, Cryptofolio tracks the mechanics specific to each protocol. Rebasing tokens, exchange-rate tokens, and auto-compounding positions are each handled according to their on-chain behavior. If a protocol is not yet supported, Cryptofolio flags the transaction for review so you can classify it manually. Once support is added, the manual entry is automatically replaced with verified on-chain data.

Staking rewards are inventory. Track them like it.

Cryptofolio creates a separate tax lot for every staking reward, at the correct FMV, in the right wallet's FIFO queue. Your income is accurate. Your lot queue is correct. Your P&L is real.

Why This Matters Beyond Taxes

Even if you are not thinking about taxes, untracked staking rewards corrupt your portfolio numbers.

Your P&L is wrong because the tracker does not know the cost basis of tokens you received as rewards. When you sell them, it either assigns zero basis (overstating your gain) or ignores them entirely (understating your holdings).

Your income is invisible. If you earned $3,000 in staking rewards over the year but your tracker did not record them as income events, your portfolio shows $3,000 in gains that are actually income. The distinction matters because income and capital gains are taxed at different rates.

Your performance metrics are misleading. A tracker that does not separate staking income from price appreciation cannot tell you how much of your return came from yield versus market movement. You might think your portfolio is up 30% from price gains when half of that is staking income you would have earned regardless of market direction.

The Bottom Line

Staking rewards are the most frequent cost-basis-creating events in most DeFi portfolios. Every reward is a new lot with its own basis and holding period. If you are staking across multiple wallets and protocols, you are generating hundreds of these per year.

Most trackers either ignore them, lump them together, or record them at the wrong time. The result is a portfolio with the wrong income figures, the wrong lot queue, and the wrong P&L on every subsequent sale.

If you are staking anywhere, check whether your tracker actually creates individual lots for each reward at the correct FMV. If it does not, every number downstream of those missing lots is built on incomplete data.

(For more on how DeFi activity affects your cost basis and tax reporting, see our DeFi tax guide, our DeFi cost basis guide, and our guide to tracking DeFi positions. For a comparison of lot accounting methods, see our FIFO vs. LIFO guide. For help evaluating whether your current tracker handles staking correctly, see our portfolio tracker guide.)

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, financial, or investment advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. The tax treatment of staking rewards, liquid staking tokens, and restaking positions involves unsettled areas of law where different tax professionals may take different positions. Consult a qualified professional for advice on your individual circumstances.