How the New Wallet-by-Wallet Cost Basis Rules Actually Work

As of January 1, 2025, crypto cost basis is tracked per wallet, not universally. Learn how the new rules work, why FIFO is the default, and where trackers fail.

For years, the standard way most crypto holders and most trackers calculated cost basis was to pool everything. If you held ETH on Coinbase, ETH on a Ledger, and ETH in MetaMask, your tracker treated all of it as one big pile. When you sold, it pulled basis from whichever lot made the math work.

That approach is no longer allowed. As of January 1, 2025, the IRS requires cost basis to be calculated per wallet and per account. Your Coinbase ETH has its own basis. Your MetaMask ETH has its own basis. They don't talk to each other anymore.

Most trackers still work the old way. Here is what changed, what the new rules actually require, and where everyone is going to get this wrong on their 2025 return.

The Rule Change

Treasury published final regulations in mid-2024 that took effect January 1, 2025. The regulation that matters here is Treasury Reg. §1.1012-1(j). It made two changes. First, every wallet and every exchange account is treated as its own separate cost basis ledger. Second, FIFO (first in, first out) is now the default method within each ledger unless the taxpayer specifically identifies which lot is being sold before the sale happens.

The old universal method let a holder who used HIFO (highest in, first out) reach across every wallet they owned and pick the lot with the highest basis to minimize taxable gain. That workaround is dead. HIFO and LIFO are still allowed, but only as forms of specific identification, only within a single wallet, and only with proper pre-sale documentation.

Alongside the regulation, the IRS issued Rev. Proc. 2024-28. It provides a one-time transitional safe harbor for taxpayers who used universal tracking before 2025 and need to allocate their basis across wallets as of January 1, 2025.

What This Looks Like in Practice

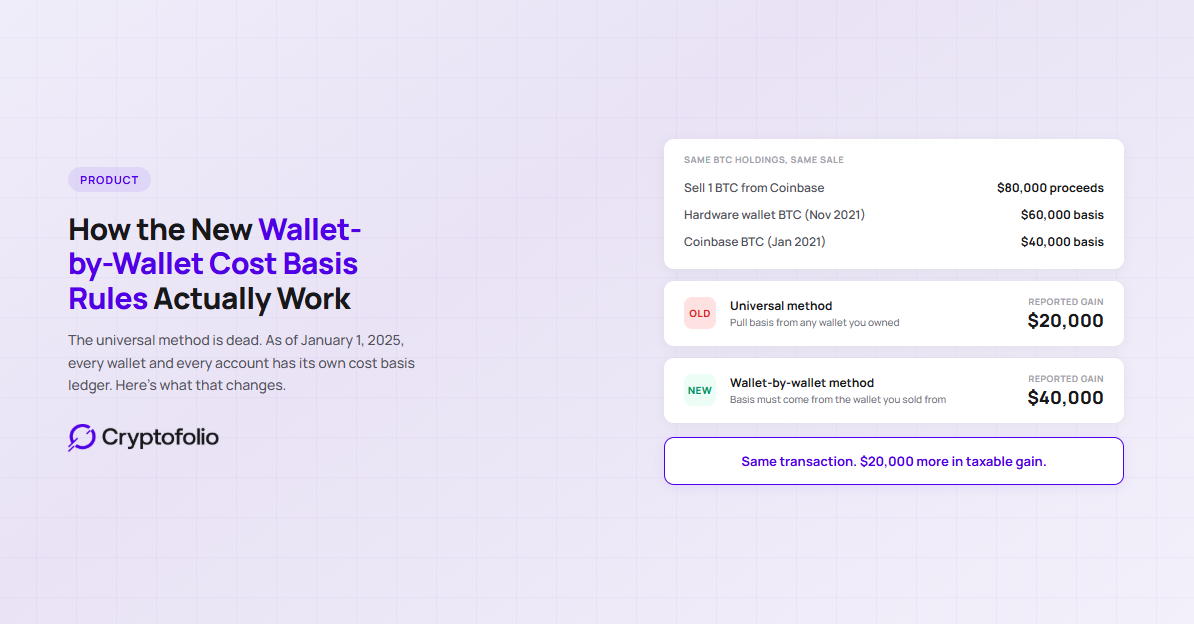

Say you bought 1 BTC on Coinbase in January 2021 at $40,000 and 1 BTC in a hardware wallet in November 2021 at $60,000. Under the old rules, if you sold 1 BTC from Coinbase in 2025 at $80,000 and used HIFO across all your holdings, your tracker could have pulled the $60,000 hardware wallet basis to minimize your gain. Reportable gain: $20,000.

Under the new rules, the BTC you sold came from Coinbase, so the basis has to come from Coinbase. Reportable gain: $40,000. The $60,000 basis in the hardware wallet stays in the hardware wallet until you sell the coin that's actually there.

This is not a theoretical change. For holders with significant BTC or ETH spread across multiple places, the difference between universal and wallet-by-wallet tracking can shift reported gains by tens of thousands of dollars on a single tax return.

The Safe Harbor Window

Rev. Proc. 2024-28 included a one-time safe harbor that let taxpayers reallocate their unused basis across their wallets as of January 1, 2025. The idea was that some wallets would end up with too much basis and others with not enough, and the safe harbor gave people a chance to fix it before the new rules locked everything in.

For specific unit allocation, the deadline is the earlier of your first 2025 digital asset disposition or the due date of your 2025 return, including extensions. For global allocation, the written rule had to be established before January 1, 2025, and the allocation completed by the same earlier-of deadline.

If you have not yet sold any crypto in 2025 and you file on extension, the final window to make a safe harbor allocation runs to October 15, 2026. If you sold anything in 2025, it closed the moment you sold. Once you miss it, you are locked into whatever basis allocation existed in your wallets on January 1, 2025. The IRS will not let you retroactively move basis from one wallet to another to reduce your tax bill.

FIFO Is the Default Nobody Wants

FIFO means the first coin you bought is the first coin you are treated as selling. In a rising market, FIFO usually produces the highest taxable gain because your oldest lots are also your cheapest lots. For a long-term holder, this is not ideal.

The alternative is specific identification. You pick exactly which lot you are selling before the sale happens. For self-custody, that means documenting the selection in your own books and records before the transaction. For broker-held assets, the permanent rule requires you to communicate the identification to the broker at or before the time of sale. Looking at your trades at tax time and declaring "I meant to sell the expensive lot" is not allowed under the permanent rule.

There is a transitional exception. Notice 2025-7, extended by Notice 2026-20, gives taxpayers a break for broker-held assets through December 31, 2026. During this window, you can satisfy specific identification by recording the selection in your own books and records before the sale, without communicating it to the broker. This applies only to assets held by custodial brokers. Self-custody has always required pre-sale documentation on your own books. The permanent specific identification rule returns January 1, 2027.

Why Most Trackers Are Still Wrong

The change broke the internal architecture of most crypto tax software. Trackers that were built around a universal ledger need fundamentally different plumbing to track each wallet as its own cost basis pool.

Here is where the breaks show up. A tracker that shows one portfolio-wide cost basis number for your ETH is using universal accounting under the hood, even if it labels the output differently. A tracker that lets you "optimize" your gains at year-end by picking the best-performing lots across all wallets is still applying the old universal method. A tracker that imports your CSV exports and produces a single FIFO number is not wallet-aware.

The 2025 tax year is the first time this matters on an actual filing. The 2026 tax year will be the first with mandatory broker cost basis reporting on Form 1099-DA for covered assets. When the numbers your tracker produces don't match the numbers your broker sends to the IRS, you have a reconciliation problem that didn't exist before.

How Cryptofolio Handles This

Cryptofolio was built from the ground up with per-wallet, per-account cost basis tracking. Every lot you acquire stays attached to the wallet or exchange where you acquired it. When you sell, the cost basis comes from that specific ledger.

FIFO is applied within each wallet by default. Specific identification is supported where the underlying exchange or wallet type allows pre-sale lot selection.

For holders who had multiple wallets at the start of 2025, Cryptofolio tracks the pre-2025 unused basis allocation alongside post-2025 acquisitions so your records reflect what the safe harbor actually produced.

Wallet-by-wallet cost basis is the rule now. Your tracker should already work this way.

Cryptofolio tracks every lot at the wallet and account level from the start. Your 2025 numbers will match what the IRS expects.

The Bottom Line

The wallet-by-wallet rule is the biggest structural change in crypto tax accounting since Notice 2014-21 established crypto as property. It took effect January 1, 2025. Most holders are now filing their first return under it, and most trackers have not been rebuilt to reflect it.

FIFO within each wallet is the default. Specific identification is allowed, but only with pre-sale documentation. The universal method is gone. If your tracker still pools your holdings into one ledger, your 2025 numbers are going to be wrong, and when the 1099-DA data catches up in 2026, the mismatch is going to show up on the IRS side.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, financial, or investment advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. While we strive to keep our content accurate and up to date, information in this article may become outdated as policies evolve. Consult a qualified professional for advice on your individual circumstances.