You Can Write Off Your Crypto Losses Against Your Stock Gains. Here's the Rule.

Yes, crypto losses offset stock gains dollar for dollar. Learn the netting order, the $3,000 deduction, wash sale quirks, and the PARITY Act risk in 2026.

If you lost money on crypto this year and made money on stocks, you can use the crypto losses to cancel out the stock gains. Dollar for dollar. It works in reverse too.

Most crypto holders don't realize this. They assume crypto and stocks sit in separate tax buckets. They don't. The IRS treats both as capital assets, which means losses on one can reduce taxable gains on the other.

The rule is simple. The details of how the math runs have one or two edges worth knowing. And there's a wash sale quirk that still works in crypto's favor in 2026, though that may not last.

The Basic Rule

A capital loss is a capital loss, regardless of which asset produced it. Sell 1 BTC at a $5,000 loss, sell $5,000 worth of Apple stock at a $5,000 gain, and your net capital gain for the year is zero. You owe nothing on that Apple gain.

This works because the IRS classified crypto as property in Notice 2014-21. Property held as an investment is a capital asset. Stocks and bonds are also capital assets. Form 8949 has one section for short-term sales and one for long-term sales. Crypto goes in the same sections as everything else. When you run the totals at the bottom of Schedule D, losses and gains from both assets are already mixed together.

There is no “crypto bucket” and no “stock bucket” on a US tax return. There is a short-term bucket and a long-term bucket, and everything a taxpayer sells during the year goes into one or the other.

How the Math Actually Runs

The IRS runs the numbers in a specific order. Short-term losses cancel short-term gains first. Long-term losses cancel long-term gains first. Then any excess in one category crosses over to the other.

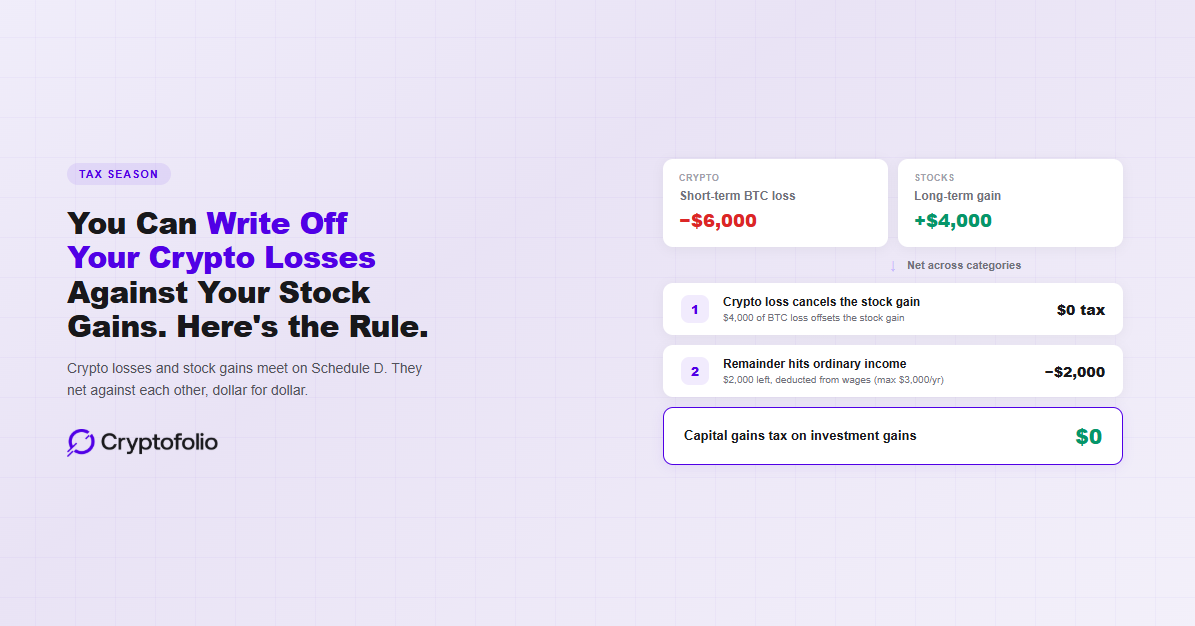

Here's what that looks like in practice.

Say you sold BTC for a $6,000 short-term loss (you held it less than a year) and also sold a long-term stock position for a $4,000 gain (you held it more than a year).

Step one: short-term losses net against short-term gains. You had no short-term gains, so the $6,000 loss carries forward to step two.

Step two: the $6,000 short-term loss now crosses over and cancels the $4,000 long-term gain. You have $2,000 of net loss left.

Step three: you can deduct up to $3,000 of net capital losses against ordinary income per year. Your $2,000 fits under the cap, so you subtract the full amount from your wages or other ordinary income.

Final result: zero tax on the $4,000 stock gain, and $2,000 off your taxable ordinary income. If you're in the 24% bracket, that's $480 of tax saved on the ordinary income side on top of the canceled gain.

If the loss had been bigger, say $15,000, the math would look like this: $4,000 cancels the stock gain, $3,000 comes off ordinary income, and the remaining $8,000 carries forward to next year indefinitely.

The Wash Sale Quirk

When you sell a stock at a loss and buy the same stock back within 30 days before or after the sale, the IRS disallows the loss under IRC §1091. This is the wash sale rule, and its window covers 30 days on either side of the sale (61 days total).

Section 1091 applies to stock or securities. It does not currently apply to crypto. The IRS treats crypto as property, and the statute is written to cover stocks and securities only. As of April 2026, this has not changed.

What that means in practice: you can sell BTC at a $5,000 loss on Monday, buy the same BTC back on Tuesday, and still claim the loss. A stock investor doing the same thing with Apple would have the loss disallowed.

Two caveats worth flagging. First, the PARITY Act is a bipartisan discussion draft that would extend wash sale rules to digital assets. A revised version was released on March 26, 2026, but it is still a discussion draft, not law. If it passes, the crypto wash sale advantage closes. Second, spot Bitcoin ETFs like IBIT sit in a genuinely unresolved area. They are structured as grantor trusts, which technically means the investor is treated as owning the underlying Bitcoin property. Some tax professionals argue §1091 should not apply. But many broker-dealers report ETF transactions on Form 1099-B and apply wash sale adjustments anyway. The IRS has not issued direct guidance. If you are trading spot Bitcoin ETFs, treat this as a gray area and expect your broker's treatment to differ from direct Bitcoin.

The broader point: harvesting crypto losses and repurchasing quickly is a legitimate strategy in 2026 that is not available on stocks. It might not be legitimate in 2027 if Congress moves on the PARITY Act.

What Counts as a Loss

A capital loss only happens when you actually dispose of the asset. That means a sale, a swap for another crypto, or using the crypto to buy something. Holding a coin that went from $100 to $10 is not a deductible loss. It's an unrealized loss on paper.

A common mistake is assuming that “my BTC is down 40%” means you can write something off. It doesn't. You have to sell or exchange the BTC first.

Another common mistake is assuming crypto that went to near-zero in your wallet can be deducted as worthless. Under a January 2023 IRS memorandum, a coin that still trades on any exchange is not considered worthless even if the price is below one cent. The practical workaround is to sell for whatever fractional amount you can get. The sale triggers a real capital loss. Holding the near-worthless coin gets you nothing.

Special Case: Losses Larger Than Gains

If your total capital losses for the year exceed your total capital gains, you deduct up to $3,000 of the net loss against ordinary income (or $1,500 if married filing separately). Anything over $3,000 carries forward to future years with no expiration.

That carryforward retains its character. A long-term loss carried forward stays long-term in the next tax year. A short-term loss stays short-term. This matters because the netting order in future years will treat it accordingly.

There's no limit on how much capital loss you can carry forward, and there's no limit on how long you can carry it. A $50,000 net loss in 2026 could take years to fully absorb, and that's fine.

How Cryptofolio Handles This

Cryptofolio tracks every realized loss as it happens, not just at tax time. You see your realized gains and losses year-to-date across every wallet and exchange, with short-term and long-term separated automatically. Cost basis flows through from the original purchase, so a $5,000 capital loss on BTC actually reflects what you paid, not what the tracker assumed.

For anyone who's sitting on gains in a brokerage account and unrealized losses in crypto, that real-time view is the practical starting point for any loss harvesting decision.

See every realized loss across every wallet in real time.

Most trackers show your balance. Cryptofolio shows you exactly what you've made, what you've lost, and what's still on the table.

The Bottom Line

Crypto losses and stock gains aren't in separate universes. They meet on Schedule D, they net against each other, and they can save you real money when the timing lines up.

Short-term losses cancel short-term gains first. Long-term cancels long-term. Anything left over crosses categories, then absorbs up to $3,000 of ordinary income per year, then carries forward indefinitely. The wash sale rule hasn't caught up to crypto yet, which means harvesting a loss and rebuying the same coin still works in 2026.

Most crypto holders leave this benefit on the table because they never connect the two sides of their portfolio. If you've got stock gains showing and crypto positions underwater, the loss is only worth something if you actually realize it.

Disclaimer: This article is for informational purposes only and does not constitute legal, tax, financial, or investment advice. Cryptocurrency tax rules are complex, depend on your specific situation, and are subject to frequent regulatory changes. While we strive to keep our content accurate and up to date, information in this article may become outdated as policies evolve. Consult a qualified professional for advice on your individual circumstances.